This text is a part of your SHN+ subscription

The senior dwelling business’s best-ever interval of occupancy, margins and income development is correct in entrance of it in 2025.

This was the prevailing sentiment that I took away from the current American Seniors Housing Affiliation (ASHA) convention, the place optimism abounded amid speak of surging occupancy and margins, the likes of which haven’t been seen in a very long time. Current studies from Inexperienced Road Advisors and NIC equally paint an image of large alternative and a coming interval of sturdy efficiency.

However whereas there was palpable pleasure for the long run at ASHA, classes from the previous additionally solid a shadow. The Nice Monetary Disaster in late 2007 and 2008 was a interval during which many senior dwelling operators want they might have been bolder, figuring out what they know now. In 2025, the senior dwelling business is approaching the same interval – and this time round, the chance is perhaps even better. Anybody analyzing the market has recognized for years that demographically-driven demand could be attributable to hit, however the alternative created by that demand has been super-charged by the occasions of the previous few years, which have paired rising demand with a drop-off in new stock.

Final yr, senior dwelling development begins reached a low not seen for the reason that monetary disaster in 2008. Though operators in 2025 are challenged to develop through new growth for a brand new era of older adults, the silver lining to that problem is that persistent low provide will nearly absolutely result in occupancy beneficial properties throughout the board within the coming months.

On the identical time, the quantity of demand forward can be now a lot better than it was greater than a decade in the past. Within the 5 years after the Nice Monetary Disaster, the inhabitants of individuals aged 80 and older within the U.S. grew 4%, in response to a stat just lately cited by Ventas (NYSE: VTR) Govt Vice President of Senior Residing Justin Hutchens. Between now and 2030, the inhabitants of individuals aged 80 and older is predicted to develop 27%.

In different phrases, the senior dwelling business has maybe by no means had such a great alternative in entrance of it because it does now during which to develop occupancy, margins and NOI.

That was additionally my impression after assembly with operators and attending periods on the ASHA convention in Phoenix final week. I feel Cogir USA CEO Dave Eskenazy summed it up greatest when he instructed me that the present slowdown in new provide represents a second of reduction for senior dwelling operators who have to catch up.

“There’s quite a lot of optimism on behalf of the operators, as a result of I feel we are able to see the sunshine now on the finish of the tunnel,” he stated.

The flip facet of that chance is that, similar to in 2008, firms threat lacking out on this demand in the event that they don’t develop and evolve to satisfy it.

On this members-only SHN+ Replace, I analyze NIC and Inexperienced Road knowledge together with my current conferences and periods from the ASHA convention and supply the next takeaways:

- Knowledge and developments displaying the senior dwelling business’s alternative is certainly large

- How operators are gearing as much as seize that chance

- Why the business might be buying and selling short-term success for issues down the highway if operators don’t work out a option to develop

Taking occupancy to 90% and past

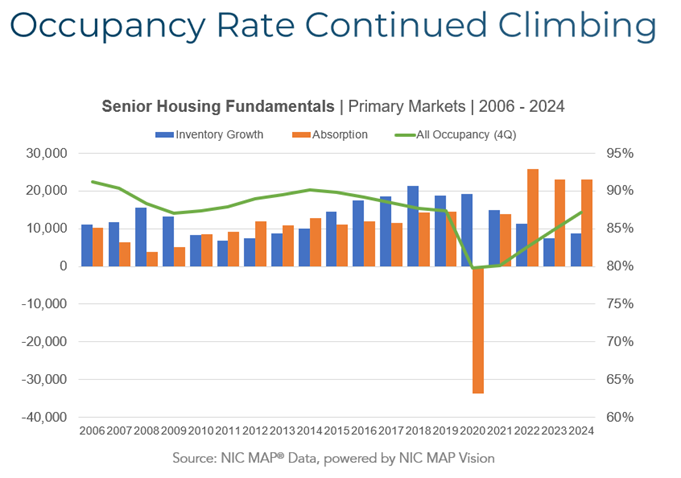

If the years after the Nice Monetary Disaster had been like a semi-final playoff recreation for the senior dwelling business, 2025 and the years to observe might be the Tremendous Bowl. One wants solely look by way of historic NIC knowledge to see what the business has to sit up for within the subsequent few years.

Between 2006 and 2009, stock development exceeded absorption. Then, as challenges growing and constructing precipitated the variety of new communities coming on-line to dwindle, absorption of items started to exceed new stock. Consequently, occupancy rose between 2009 and 2014.

Between about 2014 and 2020, the senior dwelling business entered into one other interval the place new stock eclipsed absorption, and occupancy declined accordingly, NIC MAP knowledge reveals. In 2020, absorption plummeted with the arrival of Covid-19. However absorption has far surpassed stock development in the previous few years.

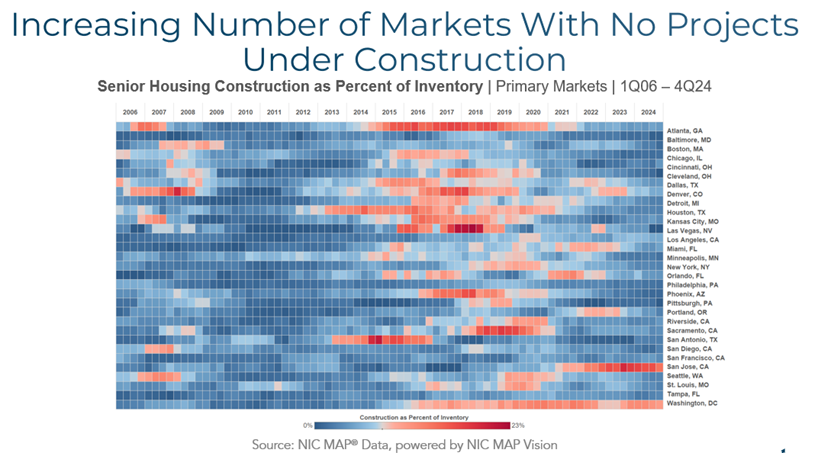

As of NIC MAP’s most up-to-date tally, development had fallen to the bottom ranges for the reason that first quarter of 2014, whereas the business’s whole variety of occupied items reached a brand new excessive watermark. And in 2024, 4 of the 31 major markets NIC MAP tracks reported no present senior dwelling development tasks, a rise over only one such market in 2023.

Evaluating the interval after the Nice Monetary Disaster and now, the senior dwelling business is in a a lot better place to regain occupancy. And certainly, occupancy is surging proper now – in 2024 alone, occupancy elevated 2.2 share factors, touchdown at 87.2% by yr’s finish.

By the top of 2025, NIC MAP believes occupancy charges might exceed 90%, an occasion that has solely occurred “a handful of occasions” for the reason that group started monitoring senior dwelling occupancy knowledge almost 20 years in the past.

In fact, as they are saying, hindsight is 20-20. And it’s clearly no secret that the business faces a years-long demand runway forward because the child boomers arrive en masse.

Within the coming yr I do see that the senior dwelling business is approaching a really distinctive alternative during which to get on higher monetary footing through occupancy and margin beneficial properties – if operators transfer to take that chance. And to that finish, I do see senior dwelling firms gearing as much as do all they will now to realize occupancy within the coming years, but in addition to set themselves up for continued success when market circumstances ultimately change.

‘Exceptionally good’ years forward, however subsequent cycle looms

In response to a Jan. 30 Inexperienced Road report, accelerating demand, minimal provide ought to spell constant occupancy beneficial properties by way of 2029, when the monetary evaluation agency expects common senior dwelling occupancy to achieve mid-90% ranges of occupancy.

The report’s authors additionally famous that builders will resume constructing “as soon as economics pencil,” however that they count on comparatively restricted provide development of round 2% by way of 2028.

To Inexperienced Road, the business’s glass is “three-fourths full” at first of 2025.

“Whereas each space of actual property comes with some dangers, the positives are more likely to outweigh the negatives for the senior housing business within the close to time period as fundamentals stay sturdy because of the vital demand versus provide imbalance,” the report’s authors wrote. “Over the long-term, decrease provide obstacles and outsized cap-ex wants might weigh on returns relative to different areas of actual property.”

And demand remains to be within the “early innings,” with years left to play out forward.

“The senior housing business is now to start with phases of an enormous demand tailwind, largely pushed by a pointy acceleration within the aged inhabitants,” the Inexperienced Road report reads. “The expansion in 80+ year-olds is predicted to decelerate all through the 2030s however largely stay north of three%, which suggests a sustained runway of demand for all types of senior housing so long as shopper preferences to reside in a senior care facility stays intact.”

Operators may also really feel the wind at their again. For instance, Legend Senior Residing CEO Tim Buchanan instructed me at ASHA he sees “a discipline of alternative proper now” given the business’s present provide and demand profile.

“The subsequent few years are going to be, I feel, exceptionally good, due to the restrict of latest development, and absorption will observe,” he instructed me.

However he added that the cycle “gained’t final eternally,” and thus it is necessary for operators to be “out in entrance of it and in a position to capitalize on the alternatives that come our manner.”

Equally, Cogir’s Eskenazy sees the business returning to a “sense of normalcy” with regard to occupancy and demand within the coming years.

Each Legend and Cogir have grown alongside bigger companions in recent times, together with by way of administration contracts with house owners together with Welltower (NYSE: WELL). And that’s the place each firms are focusing their fireplace for now as new growth stays robust. Legend, for instance, has added 21 communities to its portfolio by way of administration alternatives since 2023, whereas Cogir has almost doubled its portfolio within the U.S. since merging with Cadence Residing in 2022.

On that entrance, there appear to be much more alternatives to work with house owners together with Welltower, with such corporations implementing new methods of deploying capital as investor curiosity in senior dwelling grows. Final week, Welltower introduced the launch of a brand new non-public funds administration enterprise, which is buying NorthStar Healthcare Earnings and 40 communities in a $900 million transaction. And as CEO Shankh Mitra has identified previously, the corporate is at all times trying to find new working companions to steward good leads to its rising variety of communities.

But, it’s hanging to me that the senior dwelling business remains to be basically buying and selling the identical communities amongst operators, at the least within the quick time period. I feel that if present developments maintain, operators will return to extra wholesome occupancy and income profiles supplied they will appeal to the subsequent era of older adults. However they might be promoting themselves quick for the subsequent actual property cycle in the event that they don’t additionally discover methods to develop now earlier than one other growth growth comes.

“The optimism and nice alternative might be a cycle,” Buchanan stated. “Should you look out 10 years, there’s most likely going to be one other massive growth cycle.”

Once more, I take into consideration what senior dwelling firms inform me they want they’d accomplished within the years after 2007 and 2008. Profitable firms moved the ball ahead with inventive new ideas and fashions and reaped the advantages.

As I famous a couple of weeks in the past, I feel the senior dwelling business has one other massive alternative forward to be extra inventive and develop new fashions, together with in sectors like residence well being, PACE and the middle-market. However similar to the 5 years after the Nice Recession, that can require firms to take dangers and press by way of a cloud of uncertainty in regards to the highway forward.