Is Medicare Going Broke? What the 2026 Trustees Report Actually Says

A clear, no-panic breakdown of what the new federal report means for your coverage.

Every June, a headline shows up that is built to scare you: “Medicare is going broke.” It happened again this year, when the 2026 Medicare Trustees Report landed in Washington with the same blunt warning we have heard, in one form or another, for decades.

But here is something the scary headlines almost never explain clearly: “running short of money” and “disappearing” are two very different things. If you are 55, 65, or 75 years old, you deserve a calm, accurate explanation, not a panic button. So let us walk through what the new report actually found, what it would really mean for your coverage, and what you can do about it starting today.

What the 2026 Trustees Report Actually Found

Each spring, a small group of senior federal officials, known as the Medicare Board of Trustees, reviews the finances of the program in exact detail, the same way an accountant audits a company’s books. The 2026 edition of that report, released on June 9, contained three findings worth knowing.

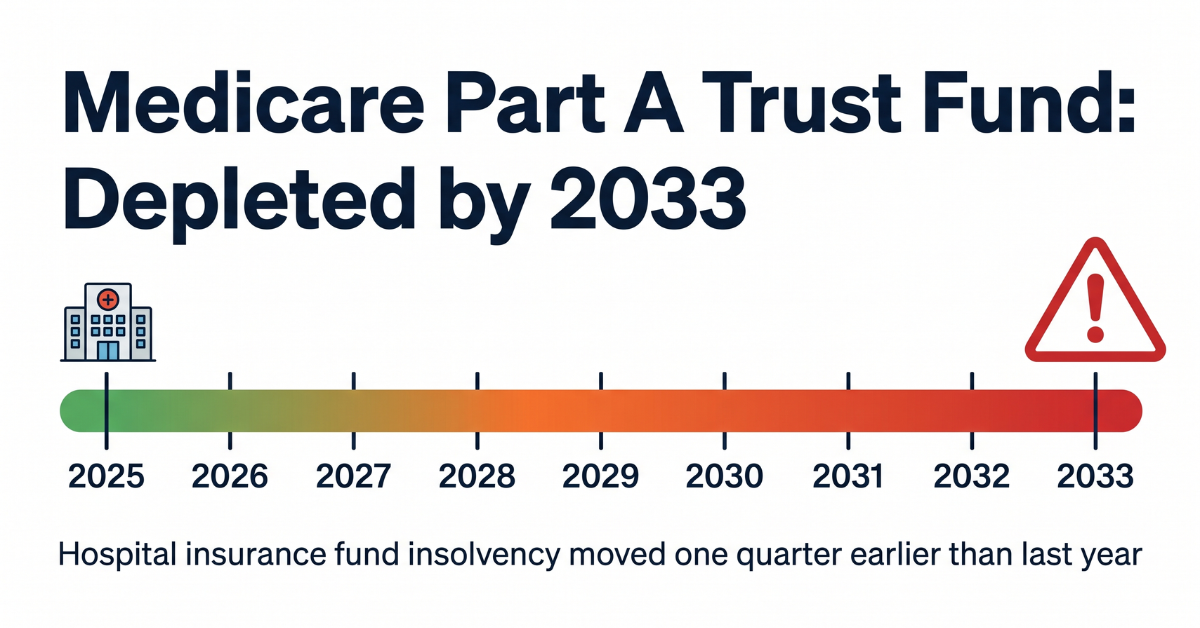

- The Hospital Insurance Trust Fund, which pays for Part A, is now projected to run short of money in 2033 — one quarter sooner than last year’s projection.

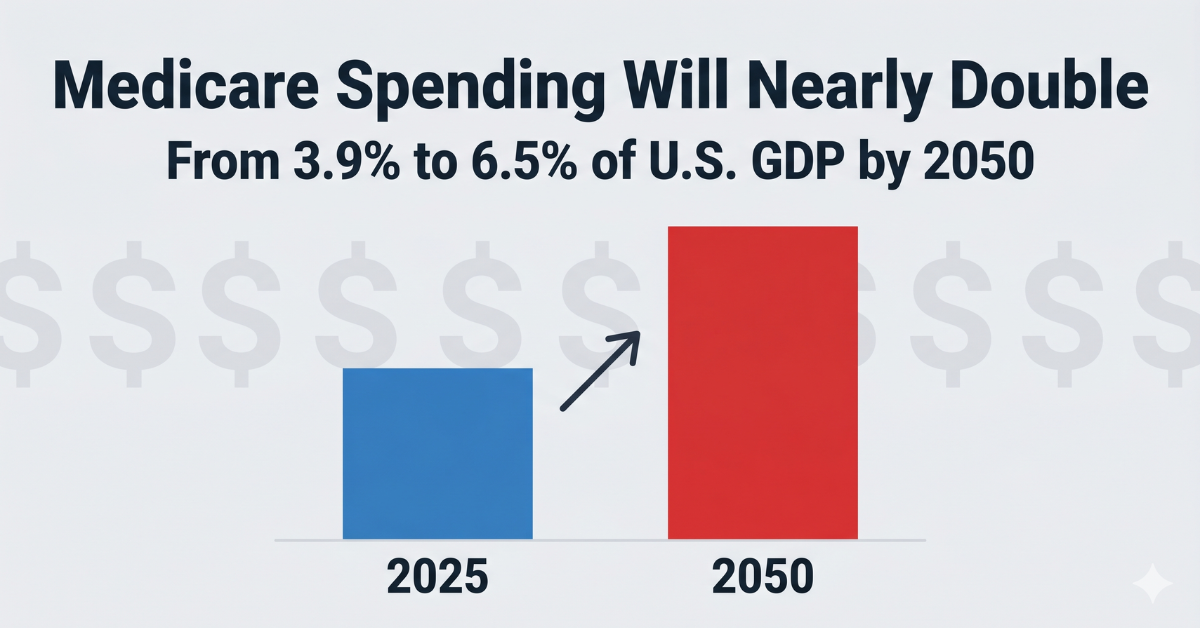

- Total Medicare spending is expected to nearly double as a share of the US economy over the next 25 years, rising from 3.9% of GDP in 2025 to roughly 6.5% of GDP by 2050.

- The fastest-growing costs are tied to care that older, frailer beneficiaries rely on most: skilled nursing facilities, home health, and hospice services.

None of this is brand new. Medicare’s trustees have flagged the same general trend for years. What changed this year is mostly the timeline moving slightly closer, driven by an aging Baby Boomer generation and rising health care costs across the board.

Will My Medicare Benefits Disappear in 2033?

This is the question that keeps people up at night, and the honest answer is: almost certainly not in the way the headlines imply.

Under current law, if the Hospital Insurance Trust Fund actually reached the point of depletion, Medicare would not simply shut off. Instead, payments to hospitals and other providers would automatically be reduced to whatever level the incoming payroll tax revenue could support. The trustees estimate that reduction at around 11% initially, growing to roughly 16% by 2040 if Congress takes no action at all between now and then.

In plain English: your Medicare card would still work. What would change first is how much Medicare pays hospitals and skilled nursing facilities, which could eventually affect access or wait times if providers respond by limiting how many Medicare patients they accept.

It is also worth knowing that Part B, which covers doctor visits, and Part D, which covers prescription drugs, work very differently from Part A. They are financed mainly through monthly premiums and general federal tax revenue rather than a fixed trust fund, so they cannot become “insolvent” in the same sense. That is genuinely good news, although it does mean their costs are passed along more directly through premiums over time.

Your 3-Step Action Plan to Protect Your Medicare Coverage Now

Worrying about Washington does not change anything. Taking a few concrete steps this year, however, absolutely can. Here is a simple plan built for exactly this situation.

Step 1: Review Your Plan Every Single Open Enrollment Period

Medicare Advantage and Part D plans change their benefits, premiums, and provider networks every year. A plan that fit you perfectly in 2024 may no longer be the best option in 2026. Block 30 minutes during the fall Open Enrollment window (October 15 to December 7) to compare your current plan against at least two alternatives using Medicare’s official Plan Finder tool.

Step 2: Find Out What Supplemental Benefits You Already Have

Here is something most people miss entirely: many Medicare Advantage plans include extra benefits beyond what Original Medicare covers, including an Over-the-Counter (OTC) allowance for everyday health essentials. This allowance often resets every quarter, and unused balances simply expire unclaimed. Before assuming your benefits are limited, it is worth checking exactly what is sitting on the table.

📋 Are You Leaving Medicare Benefits Unused?

A surprising number of Medicare Advantage members never claim their full Over-the-Counter allowance, supplemental wellness perks, or other built-in benefits — and those dollars simply disappear at the end of the cycle. Before you assume your coverage is shrinking, take two minutes to see exactly what your plan already includes.

See What’s Included In Your Plan →Step 3: Build a Small Cushion of Your Own

Even in the most pessimistic scenario, a modest personal safety net makes a real difference. If you are still working, a Health Savings Account (HSA) lets you set aside pre-tax dollars for medical costs in retirement. If you are already retired, talk with a fee-only financial advisor about whether a Medigap (Medicare Supplement) policy or a dedicated health care savings bucket makes sense for your situation. The goal is not to predict exactly what Congress will do. It is to make sure you are not depending on a single source for your peace of mind.

Staying Healthy Matters More Than Ever

Policy debates in Washington can take years to resolve. Your daily habits do not have to wait for anyone’s vote. While lawmakers argue over funding formulas, focusing on the parts of your health you can control today is one of the most powerful things you can do for your long-term independence.

Daily Nutrition Foundations

Most adults over 50 fall short on at least a few key nutrients from diet alone, especially calcium, vitamin D, and B12 — three nutrients tied directly to bone strength, energy, and cognitive sharpness. A quality multivitamin formulated specifically for this stage of life can help close that gap without overcomplicating your routine.

Most Women Over 50 Are Missing These Nutrients Every Single Day

Bone density, heart function, and brain sharpness do not wait for your next checkup to start declining. Centrum Silver Women 50+ is formulated specifically to support the nutrients women over 50 are most likely to be missing — bone strength, heart health, and brain function — in one tablet a day. No guesswork required.

Check Today’s Price on iHerb →As an affiliate, SeniorJourneyBlog may earn a commission from qualifying purchases.

Heart and Brain Support, Without the Guesswork

Omega-3 fatty acids are among the most studied nutrients for supporting cardiovascular and cognitive health in adults over 50, yet most people get nowhere near enough from diet alone unless they eat fatty fish several times a week.

Your Heart Doesn’t Get a Retirement Plan — Give It the Support It Deserves

While Washington debates trust fund timelines, your cardiovascular system is working every single second of every single day. Sports Research Alaskan Omega-3 Fish Oil is sourced from wild-caught Alaskan fish for purity and potency, delivering the EPA and DHA your heart and brain rely on most. Don’t wait for a wake-up call to start taking care of the engine that keeps you going.

Check Today’s Price on iHerb →As an affiliate, SeniorJourneyBlog may earn a commission from qualifying purchases.

What Could Happen If Congress Doesn’t Act

Lawmakers have known about this timeline for years, and several different approaches are currently being debated in Washington. None of them have been agreed upon, and presenting them fairly means showing both sides of each idea.

- Raising the payroll tax cap or rate: Supporters argue this directly shores up the trust fund without touching benefits. Critics argue it raises costs for current workers and employers.

- Gradually raising the Medicare eligibility age: Supporters say it reflects longer life expectancy. Critics point out that not everyone ages or works in physically demanding jobs at the same rate, making a flat age increase feel unfair to some groups.

- Negotiating lower drug prices further: Supporters point to recent prescription drug reforms as proof this approach saves money. Critics argue it could eventually reduce incentives for pharmaceutical innovation.

- Reducing provider payments directly: Supporters call it the most direct fix. Critics warn it could push some hospitals and doctors to limit how many Medicare patients they accept.

There is no shortage of solutions on the table. What is missing, so far, is the political agreement to choose one. That is worth watching, but it is not a reason to assume the worst about your own coverage today.

The Bottom Line

The 2026 Trustees Report is a genuine warning sign, not a doomsday clock. Medicare has faced funding warnings before, and Congress has acted before the worst-case scenarios arrived every single time. The honest, useful response is not panic. It is preparation: know your benefits, use what you are entitled to, build a small cushion of your own, and take care of the body that has to carry you through whatever comes next.

If you would like these kinds of Medicare topics explained visually, step by step, our friends at the SeoulcastUSA YouTube channel break down stories just like this one in simple, easy-to-follow videos made especially for our community. We would love for you to stop by and subscribe for more guides like this.

This article is for general informational and educational purposes only and does not constitute medical, legal, or financial advice. Please consult your physician, a licensed Medicare insurance agent, or a qualified financial advisor before making decisions about your healthcare coverage or retirement finances.

💡 Frequently Asked Questions (FAQ)

Will my Medicare benefits disappear if the Trust Fund runs out in 2033?

No. Under current law, if the Hospital Insurance Trust Fund reaches depletion, Medicare would automatically reduce payments to hospitals and other providers by roughly 11%, rising to about 16% by 2040, rather than stopping coverage altogether. Your Medicare card would continue to work, though some providers might face payment pressure.

What exactly is the Medicare Hospital Insurance Trust Fund?

It is the fund that pays for Medicare Part A, covering hospital stays, skilled nursing facilities, hospice, and home health care. It is financed mainly through payroll taxes collected from current workers, similar to how Social Security is funded.

Are Medicare Part B and Part D at risk of running out of money too?

Not in the same way. Part B (doctor visits) and Part D (prescription drugs) are funded mainly through monthly premiums and general federal tax revenue, which is replenished as needed rather than drawn from a fixed trust fund. They are not projected to become insolvent, though premiums and costs are expected to keep rising.

What can I do right now to protect myself from future Medicare changes?

Review your plan’s benefits every Open Enrollment period, check whether you are using supplemental benefits like an Over-the-Counter allowance, and consider building additional savings or a Medigap policy to cushion against potential future cost increases.

🌿 Weekly wellness, health & beauty insights — straight to your inbox

Free subscription · Cancel anytime