Navigating the waters of Medicare can often feel like trying to solve a giant, high-stakes puzzle. One wrong move, and you’re not just dealing with a bit of confusion—you’re looking at financial consequences that can follow you for the rest of your life.

As someone who has spent years helping seniors navigate the complexities of financial planning and healthcare, I’ve seen firsthand how overwhelming the system can be. Whether it’s the different “Parts,” the strict deadlines, or the fine print in private plans, it’s easy to feel like you’re walking through a minefield. But here’s the reality: in 2026, the cost of making a mistake has never been higher.

Today, I want to walk you through the seven most critical Medicare pitfalls I’ve observed. By understanding these now, you can protect both your health and your hard-earned retirement savings.

1. The Lifetime Price of Procrastination: Late Enrollment Penalties

This is perhaps the most painful mistake because it is entirely avoidable, yet it happens every single year. Medicare has very strict enrollment windows, and missing them isn’t just a one-time fee—it’s a permanent hike in your premiums.

The Initial Enrollment Period (IEP) is the seven-month window around your 65th birthday. If you miss this and don’t have what the government calls “creditable coverage” (like insurance from a large employer), you will face the Part B late enrollment penalty.

In 2026, this penalty is 10% for every full 12-month period you were eligible but didn’t sign up. If you wait just two years, your monthly Part B premium will be 20% higher forever. With the standard 2026 Part B premium at $202.90, a 20% penalty means you’re paying $243.48 every month. Over 15 years, that’s over $7,300 down the drain.

My Advice: Mark your calendar three months before your 65th birthday. Even if you’re still working, verify with your HR department and Medicare.gov if your current coverage allows you to delay enrollment without penalty.

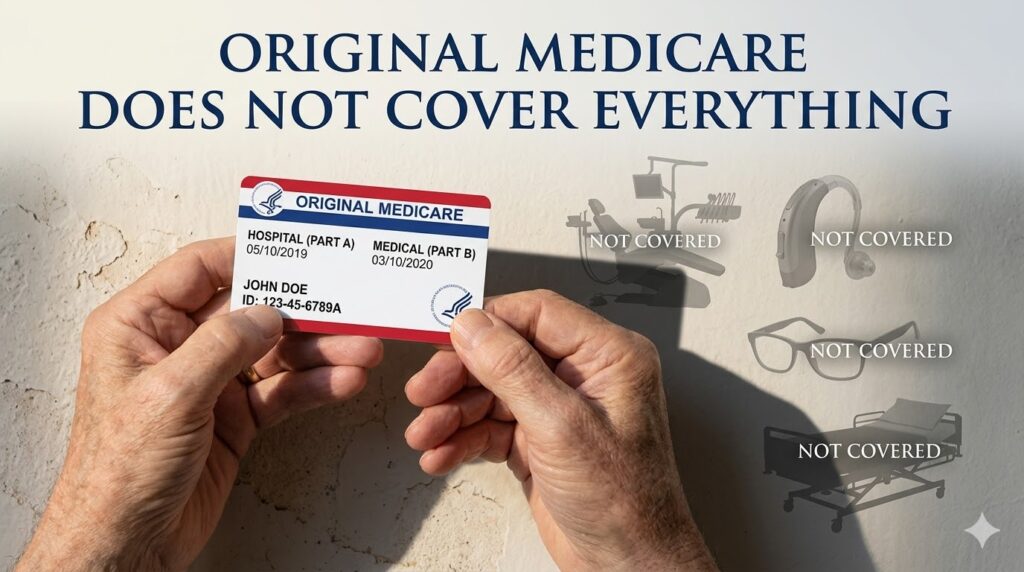

2. The Myth of “Full Coverage” Under Original Medicare

A common misconception I hear is, “I have Medicare, so I’m fully covered.” Unfortunately, Original Medicare (Parts A and B) is more like a foundation than a complete house. It leaves significant gaps that can lead to massive out-of-pocket costs.

Standard Medicare does not cover:

- Routine dental care or dentures

- Vision exams and glasses

- Hearing aids

- Long-term custodial care (nursing homes)

To put this in perspective for 2026, a full set of dentures can run between $2,800 and $4,500, and high-quality hearing aids can cost upwards of $7,000. If you rely solely on Original Medicare, you are paying every penny of that yourself. To avoid this shock, you must look into Medigap policies or Medicare Advantage plans that specifically include these “extra” benefits.

3. Picking the Wrong Part D Plan (Or Skipping It Entirely)

Prescription drug coverage, or Part D, is another area where a “set it and forget it” mentality will cost you. Every year, insurance companies change their “formularies”—the list of drugs they cover and how much they charge for them.

In 2026, the Part D deductible can be as high as $590. For seniors on expensive specialty medications, choosing a plan that puts your drug in a higher “tier” can result in paying thousands more than necessary. I’ve seen cases where a simple plan switch saved a person $3,000 to $6,000 a year just by matching their specific medications to the right provider.

Pro Tip: Use the Medicare Plan Finder tool during the Annual Enrollment Period. Enter your exact prescriptions and your zip code. It’s the only way to ensure you aren’t overpaying.

4. Medicare Advantage vs. Medigap: The Great Debate

Choosing between Medicare Advantage (Part C) and Medigap (Supplement) is one of the biggest decisions you’ll make.

- Medicare Advantage often boasts $0 monthly premiums and includes dental/vision. It sounds like a steal, but it operates through provider networks.

- Medigap has a higher monthly premium but allows you to see any doctor in the U.S. that accepts Medicare. There are no networks to worry about.

The mistake many make is choosing Advantage solely for the low premium, only to realize later that their specialist isn’t in the network or that they need “prior authorization” for every major procedure. If you travel frequently or have a specific doctor you refuse to leave, Medigap is usually the safer, albeit more expensive, bet.

5. The Hidden Walls of Medicare Advantage Networks

Since over 54% of beneficiaries are now in Medicare Advantage, it’s crucial to talk about networks and prior authorizations.

In 2026, networks are tighter than ever. If you unknowingly go to an out-of-network hospital for a procedure, you could be billed for the entire amount. I recently spoke with a senior who received a $15,000 bill because their specialist had dropped out of their plan’s network midway through the year.

Furthermore, these plans often require the insurance company to “approve” a surgery or an MRI before it happens. If you don’t get that green light first, they can deny the claim entirely. Always call your doctors before the year starts and ask: “Will you accept this specific plan in 2026?”

6. Skipping the Annual Enrollment Period (AEP)

From October 15th to December 7th, you have the power to change your coverage. Yet, many people skip this window because they “feel fine” with their current plan.

Insurance companies bank on this inertia. In 2026, premiums and deductibles are shifting across the board. People who don’t compare plans during AEP often end up paying $500 to $2,500 more per year than they need to. Even if you love your plan, check its “Star Rating.” If it has dropped below four stars, it might be time to see what else is out there.

7. Leaving Money on the Table: Ignoring “Extra Help”

There is a program called the Low-Income Subsidy (LIS), also known as “Extra Help.” In 2026, it’s estimated that over 13 million seniors qualify for this assistance but haven’t applied.

If your annual income is under approximately $23,000 (for an individual) and you have limited assets, the government can pay for your Part D premiums, deductibles, and co-pays—often bringing your drug costs down to $0.

Many middle-class seniors feel too “proud” to apply, thinking it’s only for the destitute. It’s not. It’s a program designed to help you maintain your quality of life on a fixed income. The application takes 10 minutes at SSA.gov, and it could be the most profitable 10 minutes of your year.

Final Thoughts

Medicare doesn’t have to be a nightmare, but it does require you to be proactive. By avoiding these seven traps, you ensure that your retirement funds go toward enjoying your life, rather than paying for avoidable penalties and overpriced coverage. Take the time this year to review, compare, and lock in the best possible health future for yourself.