")

Living in California, I’ve seen countless friends, neighbors, and clients needlessly stress over Medicare deadlines, convinced the federal government is waiting to penalize them the second the clock strikes midnight on their 65th birthday. The mailbox suddenly overflows with aggressive insurance flyers, and the unsolicited phone calls seem endless. The prevailing rumor is simple and terrifying: If you don’t sign up for Medicare at 65, you will face severe lifetime financial penalties.

Here is the truth that the insurance brochures rarely explain clearly: While some people absolutely must enroll in Medicare at 65 to avoid disastrous gaps in coverage, nearly half of all seniors today are legally and safely delaying their Medicare Part A and Part B enrollment. They are doing so without paying a single dime in late penalties, and in many cases, delaying enrollment is the smartest financial move they can make.

In this comprehensive guide, we will break down exactly who is required to enroll at 65, who has the legal right to refuse, and the strategic options available to those who choose to keep working.

Who is Strictly Required to Start Medicare at 65?

Before we discuss how to delay Medicare, we must clearly define who does not have that luxury. If you fall into any of the following five categories, Medicare Part A and Part B are not optional at age 65; they are essential to protect your health and your wallet.

1. Individuals Who Are No Longer Working

If neither you nor your spouse is actively working, and you do not have access to an active employer-sponsored health plan, you must transition to Medicare. Retirement signifies the end of active group coverage, making Medicare your primary health insurance.

2. Those Currently on COBRA Insurance

COBRA is an excellent temporary safety net for maintaining your previous employer’s health coverage after you leave a job. However, the rules change drastically when you turn 65. Once you become eligible for Medicare, COBRA automatically moves to a “secondary payer” position. If you rely solely on COBRA at 65, you will effectively become the first payer for your medical bills, which could lead to catastrophic out-of-pocket expenses.

3. Military Retirees on TRICARE

TRICARE provides robust health coverage for retired military personnel. But similar to COBRA, once you hit your 65th birthday, TRICARE rules dictate that it will only pay second to Medicare. If you fail to enroll in Medicare Parts A and B, TRICARE will not step in to cover the primary costs, leaving you financially vulnerable.

4. Policyholders of Affordable Care Act (ACA) Plans

If you secure your health insurance through the Healthcare Exchange (Obamacare), turning 65 triggers a massive shift in your financial incentives. All the benefits that make an ACA plan affordable—tax subsidies, reduced premiums, and cost-sharing reductions—vanish at age 65. While you are technically allowed to keep an ACA plan, doing so means paying full, unsubsidized premiums and deductibles. Transitioning to Medicare is the only financially viable path.

5. Employees of “Small Employers” (Under 20 Employees)

If you are still working, but your company has 19 or fewer employees on the payroll, you must enroll in Medicare. The federal government classifies this as a “small employer.” In this scenario, Medicare takes the primary payer position, and your employer’s health plan becomes secondary. If you skip Medicare, your small employer’s insurance company can legally refuse to pay your primary hospital or doctor bills, arguing that Medicare should have covered them.

The One Group That Can Safely Refuse Medicare at 65

There is only one specific group of individuals who can completely bypass Medicare at age 65 without facing penalties: People who are still actively working, intend to keep working, and receive their health insurance through a “Large Employer.”

Medicare defines a Large Employer as a company with 20 or more employees actively on the payroll.

If you or your spouse meet this exact criteria, the employer’s health plan remains the primary payer. You are fully protected, and you have the right to refuse Medicare until you eventually retire or lose that specific coverage. If you are in this fortunate position, you have three distinct options for handling your healthcare at 65.

Option 1: Do Absolutely Nothing (The HSA Secret)

It sounds counterintuitive, but for many actively working 65-year-olds at large companies, the best action is total inaction. You do not need to sign up for Part A (Hospital Insurance) or Part B (Medical Insurance).

Why would you ignore a federal benefit? The answer lies in your tax strategy—specifically, if you are actively contributing to a Health Savings Account (HSA).

The Power of the HSA

An HSA is one of the most powerful wealth-building tools in the American tax code. It offers a triple-tax advantage: your contributions are tax-deductible, the money grows tax-deferred, and withdrawals used for qualified medical expenses are 100% tax-free. (Note: This applies only to HSAs, not Flexible Spending Accounts (FSAs) or Health Reimbursement Arrangements (HRAs)).

The Medicare / HSA Conflict

Here is the critical catch: If you enroll in any part of Medicare (even just Part A), you are legally prohibited from making any new contributions to your HSA. You can still keep and spend the money already in the account, but your ability to funnel new, tax-advantaged money into the HSA is permanently revoked. If you want to keep maximizing your HSA contributions during your peak earning years, you must completely refuse both Medicare Part A and Part B.

Busting the “Lifetime Penalty” Myth

You have likely heard a rumor that if you don’t sign up for Part A at 65, you will face a penalty for the rest of your life. Social Security office workers have even been known to accidentally repeat this misinformation.

This is a myth.

The only people penalized for delaying Part A are those who are required to buy Part A. That represents less than 1% of the US population. If you (or your spouse) have worked and paid FICA/Medicare taxes for at least 40 quarters (10 years) over your lifetime, your Medicare Part A premium is $0.

Medicare penalties are calculated as a percentage of your premium. If you delay Part A for five years, your penalty is a percentage of zero. Mathematically, 1,000% of zero is still zero. You will never pay a late penalty for Part A if you have your 40 working quarters.

Option 2: Enroll in Medicare Part A Only

If you are covered by a large employer plan (20+ employees) but you are not contributing to an HSA, your best strategic move is usually to enroll in Medicare Part A only, while continuing to delay Part B.

The Benefits of Part A as a Secondary Payer

For 99% of Americans, Medicare Part A is premium-free. By enrolling in it while you continue to work, your employer’s health insurance remains your primary coverage, and Medicare Part A acts as your secondary coverage for hospitalizations.

If you are admitted to the hospital, Medicare Part A will not cover your primary deductibles or co-payments. However, it can step in to cover co-insurance.

Case Study in Co-Insurance: Imagine your employer plan covers 80% of a major hospital stay, leaving you responsible for the remaining 20% co-insurance. If you have Part A active as your secondary insurance, Medicare will coordinate benefits with your employer’s plan and may cover some or all of that 20% gap. Because Part A costs you nothing in monthly premiums, it serves as a free, additional layer of financial armor against catastrophic hospital bills.

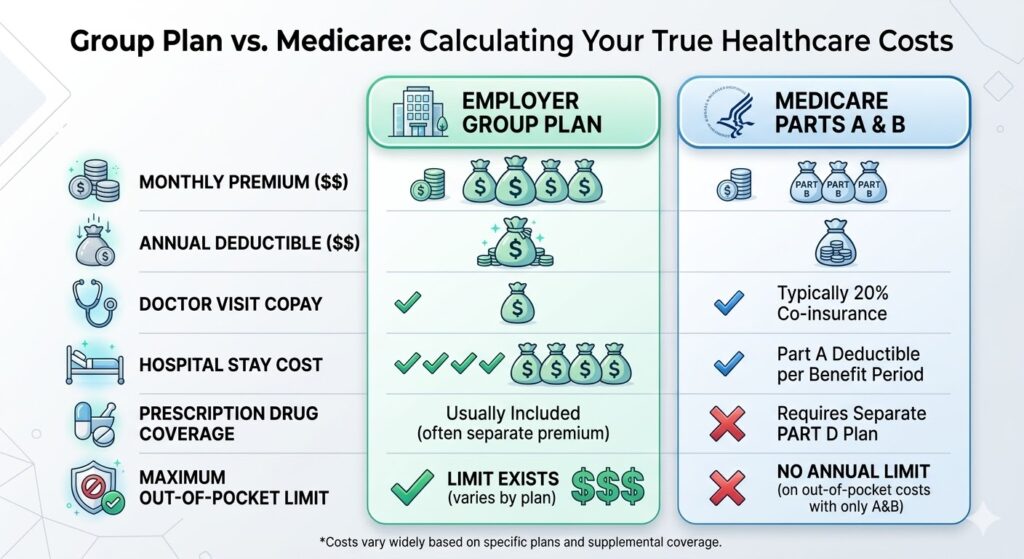

Option 3: Ditch the Group Plan for Full Medicare (Parts A & B)

Just because you can keep your large employer’s group plan doesn’t mean you should. Sometimes, employer-sponsored healthcare is, quite frankly, mediocre and expensive. If you are paying steep premiums for a plan with a massive deductible, it is time to run the numbers.

You have the right to drop your employer’s coverage at 65 and transition fully into Medicare (Parts A and B, plus a Medigap or Advantage plan and Part D).

The Cost Comparison Checklist

Before leaving a group plan, sit down and compare these five critical factors:

- Monthly Premiums: What is being deducted from your paycheck? Look closely at the “Employee Only” vs. “Employee + Spouse” costs. Often, an employer highly subsidizes the employee’s premium but charges exorbitant rates to keep a spouse on the plan (e.g., jumping from $100/month to $500/month).

- Annual Deductible: If your employer plan has a $3,000 deductible, you are effectively paying an invisible $250 per month out-of-pocket before insurance even kicks in.

- Co-Insurance Rates: Are you on an 80/20 plan? A 90/10 plan? Compare this to a Medicare Supplement (Medigap) Plan G, which covers 100% of Part B excess charges and co-insurance after a very low annual deductible.

- Maximum Out-of-Pocket (MOOP): If you were diagnosed with cancer tomorrow and required surgery, radiation, and chemotherapy, what is the absolute maximum you would have to pay on your group plan? Some employer plans have a MOOP of $10,000 or more.

- Prescription Drug Costs: Compare your current pharmacy copays with a standalone Medicare Part D plan.

A Crucial Warning About Dependents

If you decide that Medicare is a better financial deal and you leave your employer’s plan, your dependents will lose their coverage. If you carry a younger spouse who is not yet 65, or children under the age of 26 who rely on your insurance, you must factor in how they will get coverage before you make the leap to Medicare.

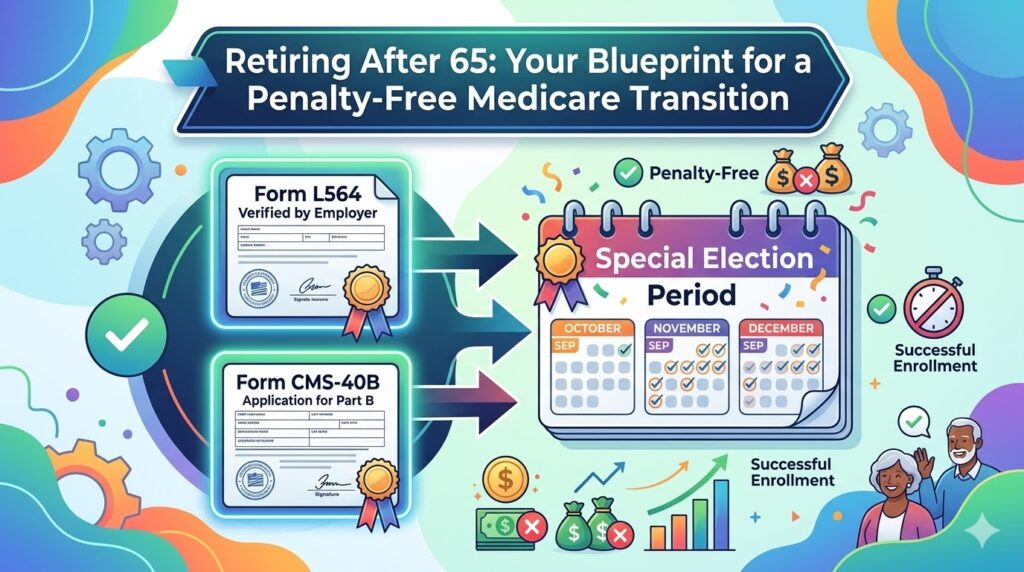

The Transition: How to Enroll Later Without Penalties

If you choose Option 1 or Option 2, there will come a day when you finally retire, or simply decide to stop working. How do you transition to full Medicare at age 68, 70, or 72 without triggering the dreaded late enrollment penalties?

You will use a Special Election Period (SEP).

Unlike the Initial Enrollment Period (IEP) that surrounds your 65th birthday, the SEP is designed specifically for people leaving credible employer coverage later in life. To successfully navigate the SEP without penalties, you must follow a strict administrative process to prove to the federal government that you maintained active, credible coverage since you turned 65.

The Two Golden Forms of the SEP

To execute this transition smoothly, you will need two specific documents:

- Form CMS-L564 (Request for Employment Information): You do not fill this out entirely yourself. You must hand this form to your company’s Human Resources department. HR will officially verify that you (or your spouse) have been actively employed and covered by a large group health plan continuously since your 65th birthday.

- Form CMS-40B (Application for Enrollment in Medicare – Part B): This is your actual application. On this form, you will indicate the exact date you want your Medicare benefits to begin (e.g., “Please begin my Medicare on August 1st”).

The 90-Day Rule and the Danger of Gaps

Timing is everything. You should submit these forms to the Social Security Administration no sooner than 90 days before your employer coverage is scheduled to end.

The absolute most critical rule of the Special Election Period is that you cannot have any gaps in coverage. If a 79-year-old retires, they must prove continuous, unbroken employment and group coverage for the 14 years since they turned 65. Even a one-month gap in coverage can derail your SEP eligibility and subject you to permanent Part B late enrollment penalties (which scale at 10% for every full 12-month period you were eligible but not enrolled).

Final Thoughts on Your Medicare Journey

Turning 65 does not automatically mean you are forced into the Medicare system. By understanding the size of your employer, the mechanics of your Health Savings Account, and the realities of Special Election Periods, you can make a strategic, data-driven decision about your healthcare future. Take the time to compare your current premiums against Medicare’s offerings, protect your dependents, and when the time finally comes to retire, ensure your L564 paperwork is flawless.

💡 자주 묻는 질문 (FAQ)

Q1: Do I have to enroll in Medicare at 65 if I am still working?

A1: Not necessarily. If you or your spouse are actively working and get your health insurance from a “Large Employer” (a company with 20 or more employees), you can safely delay Medicare Part A and Part B without any late penalties. However, if your company has fewer than 20 employees, Medicare must become your primary insurance at 65.

Q2: Will I face a lifetime penalty if I don’t sign up for Medicare Part A at 65?

A2: For the vast majority of Americans, this is a myth. If you or your spouse have worked and paid Medicare taxes for at least 40 quarters (10 years) over your lifetime, your Part A premium is $0. Because late penalties are calculated as a percentage of your premium, a percentage of zero is still zero. You only face penalties if you are among the 1% who must purchase Part A.

Q3: How do I transition to Medicare later when I finally retire without getting penalized?

A3: When you retire after 65, you will use a Special Election Period (SEP). You must submit Form CMS-L564, filled out by your employer’s HR department, to prove you maintained continuous group coverage since age 65. You will also submit Form CMS-40B to select your Medicare start date. You must apply within 8 months of losing coverage, but ideally, you should start the process 90 days before your employer plan ends to avoid any gaps.