Decoding Original Medicare: The Essential Foundation and Its Gaps

Turning 65 is an incredible milestone, a time to look back on a lifetime of achievements and forward to the adventures that lie ahead. However, for many of us, this major birthday also brings a flood of mail and a sudden, urgent question: “How do I choose the right Medicare plan?” Many seniors find this entire process overwhelming, as it feels like trying to decipher a foreign language while being pressured to make permanent, high-stakes decisions.

That shared confusion is precisely why clarity and accurate information are so vital during this transition. Clarity beats complexity every time. Our goal here at SeniorJourneyBlog is to be your trusted partner, cutting through the noise to provide precise, actionable guidance as you build your health care foundation. Facing this maze together, we can ensure you approach your enrollment with confidence, not confusion.

The first step in taming the complexity of Medicare is understanding its distinct components—often referred to as the alphabet soup of Parts A, B, C, and D. Let’s break down this fundamental structure so you can make informed choices that protect your health and your finances in this joyful new chapter of life.

Decoding Original Medicare: Parts A and B Explained

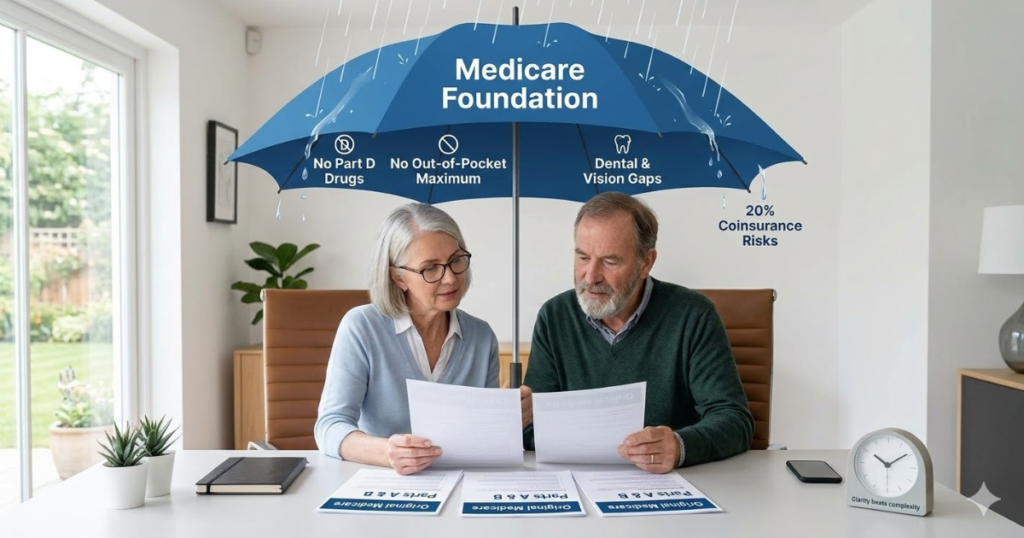

For the majority of seniors, Original Medicare is the starting line. When you turn 65, and if you are a US citizen or permanent resident, you are generally eligible for this foundational coverage. It is comprised of two core sections: Part A and Part B. Think of Original Medicare as the bedrock upon which you build further coverage, but understanding exactly what it protects—and what it does not—is absolutely critical.

Medicare Part A: The Hospital Guard

Medicare Part A is best understood as your hospital insurance. Its primary function is to protect you during some of the most expensive moments in healthcare—when you are an inpatient. This doesn’t just mean a multi-night stay for a major procedure; it covers diverse forms of institutional care.

Part A typically covers:

- Inpatient hospital care

- Skilled nursing facility care (for limited, post-hospitalization rehabilitation)

- Hospice care

- Some home health care services

Expert Tip: The vast majority of Americans do not pay a monthly premium for Medicare Part A, provided they or their spouse worked and paid Medicare taxes for at least ten years (or 40 quarters). This “premium-free” structure is a major relief for many retirees, but it’s important to remember that it is not “free” care. It still involves significant deductibles and coinsurance for each benefit period, meaning you need to understand the out-of-pocket costs before you have covered services.

Medicare Part B: Outpatient Protection

While Part A covers your care inside the institution, Medicare Part B serves as your essential outpatient and daily protection. It is your medical insurance for those services that keep you healthy on a daily basis and manage ongoing conditions outside of a hospital bed. Because Part B is comprehensive, understanding its details is vital for every senior.

Part B generally covers:

- Services from doctors and other health care providers (both inpatient and outpatient)

- Outpatient care

- Home health care

- Durable medical equipment (DME), such as walkers and wheelchairs

- Many preventive services, like screenings, vaccinations (including flu shots), and an annual wellness exam

Expert Tip: Unlike Part A, Medicare Part B always requires a monthly premium, which is generally deducted directly from your Social Security benefits if you are receiving them. The standard premium amount is set annually by the government and can be higher depending on your income (a provision known as IRMAA). It also includes an annual deductible and, most significantly, a 20% coinsurance for most services with no out-of-pocket maximum. This is the precise financial vulnerability that often drives seniors to seek additional coverage.

Why You Might Still Feel Exposed

Original Medicare, while robust, has critical gaps that can leave you with substantial, unpredictable bills. There is no prescription drug coverage. There is no coverage for most routine dental, vision, or hearing care. And, as mentioned, that 20% coinsurance on Part B has no limit, meaning a single major illness could devastate your savings. This precise limitation is the engine that drives seniors toward the choices outlined below. Clarity is paramount as you decide which path to follow to protect your wealth and well-being.

Deciding Your Medicare Path: The Final Crossroads of Medigap vs. Advantage.

Prescribing Peace of Mind: Medicare Part D Basics

Understanding how to protect your health with prescription drug coverage is a primary concern for almost every senior. Original Medicare (Parts A and B) explicitly does not cover these essential medications. This is where Medicare Part D enters the picture, designed to provide affordable access to prescription drugs that many of us rely on for chronic condition management and preventive health.

Clarity beats complexity here too. Let’s simplify how you secure this critical coverage and what to look out for.

How to Get Part D Coverage

You have two main ways to obtain prescription drug coverage:

- Stand-Alone Part D Prescription Drug Plan (PDP): If you choose Original Medicare and opt for a Medicare Supplement Insurance (Medigap) plan, you will need to enroll in a separate, stand-alone PDP provided by a private insurance company. This plan will require its own monthly premium.

- Medicare Advantage Plan with Prescription Drug Coverage (MA-PD): If you opt for a Medicare Advantage plan (which we will cover in detail), the vast majority of these private plans automatically bundle prescription drug coverage into their structure. This is often a single premium for everything.

Decoding Formularies and Tiers

Expert tip: Every Part D plan, whether stand-alone or bundled, must follow a government-defined standard, but the exact drugs covered and their costs vary dramatically from plan to plan. This is due to a plan’s unique “Formulary,” which is a tiered list of covered drugs. Understanding a plan’s formulary and its tier structure is essential to avoiding unexpected and exorbitant costs.

- Tiers: Most plans structure their formulary with tiers. Tier 1 is generally comprised of the lowest-cost generic drugs, while higher tiers (e.g., Tier 3, 4, or 5) consist of more expensive preferred brand-name or specialty medications. Your coinsurance or copay will be significantly higher for drugs on higher tiers.

- Annual Review: Your health needs change, and plan formularies can change every single year. A vital expert tip is that every senior must review their Part D plan during Medicare’s Open Enrollment period (October 15 – December 7). Failing to do so can lead to a standard penalty known as the “Donut Hole” and result in far higher drug costs for medications that may no longer be covered efficiently by your current plan. Taking just one hour to review your options can save you hundreds, or even thousands, of dollars over the coming year.

Filling the Gaps: Medicare Supplement Insurance (Medigap)

The gaps within Original Medicare (Parts A and B)—the deductibles, coinsurance, and no out-of-pocket limit—are precisely the financial risks that Medicare Supplement Insurance (Medigap) is designed to mitigate. Medigap plans are standardized, private insurance policies explicitly built to pay for those remaining costs that Original Medicare doesn’t cover. For many seniors, Medigap provides the ultimate peace of mind and financial predictability.

The Power of Standardization

A crucial point of clarity: Medigap plans are standardized by the federal government and are designated by letters (Plans A through N, although some are no longer available to new enrollees). While different private insurance companies sell these plans, the benefits of, for instance, a Medigap Plan G are identical regardless of which carrier you choose. The only meaningful difference will be the premium they charge and their history of premium stability, which makes cost accurate information absolutely paramount.

Medigap plans offer significant predictability:

- Original Medicare (A&B) remains your primary insurance. When you go to a provider that accepts Medicare (which is most), Original Medicare pays its share, and your Medigap primary insurer pays its standardized share.

- Depending on the specific plan letter you choose, your out-of-pocket costs can be almost completely eliminated, allowing you to budget with incredible accuracy. This cost predictability is the single biggest advantage of choosing a Medigap plan.

- You will have a separate, monthly premium for your Medigap plan, in addition to your Medicare Part B premium. You must also purchase a separate stand-alone Part D prescription drug plan.

Deciding for Your Lifestyle

Expert guidance: Choosing the right standardized plan, such as Plan G or Plan N, will dictate your costs. However, this path also offers maximum flexibility. You can see any doctor or specialist in the nation who accepts Medicare. You are not limited by any private carrier’s network, which is a major benefit for many of us who value choice or like to travel within the US. A detailed case study often helps make this concrete.

A One-Stop Shop: Understanding Medicare Advantage (Part C)

If Medigap is like buying a foundational truck and adding customized protection, Medicare Advantage (Part C) is like buying an all-in-one sport-utility vehicle. Medicare Advantage plans are a private-market alternative to Original Medicare. Instead of Original Medicare paying your providers directly, the federal government contracts with private insurance companies to manage and pay for your covered health care services.

When you enroll in a Part C plan, you get one-stop-shop coverage for all your Part A and Part B benefits, often bundled with additional features that Original Medicare does not cover.

Here is the essential breakdown of Part C:

- The Bundle: The vast majority of Part C plans bundle Part A, Part B, and prescription drug coverage (Part D) into a single plan. You will get one simple ID card for all your care.

- Private Networks: Most Part C plans structure their delivery through a private network of doctors and specialists, similar to the HMO or PPO plans you may have had during your working years. Understanding the private network structure is absolutely critical. Some plans (HMOs) generally require you to see providers in the network, while others (PPOs) offer more flexibility to go out-of-network, often at a higher cost.

- The Extras: Private plans compete for your business, and one way they do this is by offering “extra” benefits that Original Medicare does not. This frequently includes coverage for:

- Routine dental care (screenings, cleanings)

- Routine vision care (exams, eyeglasses)

- Routine hearing care (exams, hearing aids)

- Fitness benefits, such as a “SilverSneakers” gym membership

- Over-the-counter allowances

Expert Tip: Many Part C plans feature lower monthly premiums, and some even have a $0 premium. However, this low cost accurate information is only half the equation. You must understand the specific out-of-pocket costs (copays and coinsurance) that you will face for specific services, and crucially, the plan’s stated out-of-pocket maximum, which limits your total annual financial risk.

Piecing Together the Medicare Puzzle: Choosing a Custom-Fit over a Bundle.

The Crucial Decision: Medigap (Supplement) vs. Medicare Advantage (Part C)

This is the most impactful choice every senior faces, and it is where clarity beats complexity is most essential. The distinction between a Medicare Supplement (Medigap) plan and a Medicare Advantage (Part C) plan is fundamental to your budget, your choice of doctors, and your financial risk.

Let’s use a dynamic case study to make the expert tips concrete and demonstrate which path might best fit your unique needs. We can envision two diverse profiles: “Predictable Pat” and “Advantage Fran.”

Medigap Pat vs. Advantage Fran: A Decision Tale

Predictable Pat:

- Profile: Pat is a 70-year-old active retiree. Pat has been managing a manageable but chronic health condition that requires regular check-ups with a specific heart specialist and a trusted primary care doctor. Pat values knowing exactly what their healthcare costs will be, even with a separate premium. Pat travels frequently to visit family and values the freedom to see any doctor, anywhere.

- Medigap Choice: For Pat, a Medigap plan, such as Plan G, coupled with Original Medicare and a stand-alone Part D plan, is the ideal choice.

- Pros: Pat pays a higher, but fixed, separate premium. Pat enjoys maximum cost accurate information. Pat can see any Medicare-accepting doctor in the US.

- Cons: Pat doesn’t get the bundled extra benefits (dental, vision) in their Medigap plan and must manage these needs or purchase a separate plan.

Advantage Fran:

- Profile: Fran is 66, relatively healthy, and is motivated to simplify their coverage while keeping premiums low. Fran values convenience and is not overly concerned with cost accurate information as long as they understand their out-of-pocket maximum. Fran is happy with their local private network and the ease of a single ID card.

- Advantage Choice: A Medicare Advantage plan is the perfect “all-in-one, one-stop shop” for Fran.

- Pros: Fran gets Parts A, B, and D bundled, often for a lower combined premium than Pat. Fran enjoys convenience with one ID card. Fran gets built-in “extras” like gym memberships and dental/vision benefits that Pat does not.

- Cons: Fran is limited by a private network of doctors and specialists and must understand the potential impact on their care choice. Fran’s costs are less predictable and rely on copays and coinsurance for services, rather than a known premium, and require a full understanding of their out-of-pocket maximum.

Choosing Your Best Fit

Every decision is different, but having a clear understanding of your unique needs is paramount. Facing this maze together, you can identify the path that aligns with your health and financial goals. A final checklist often helps make this complete.

Medigap vs. Advantage: A Dynamic Summary

| Feature | Original Medicare + Medigap | Medicare Advantage (Part C) |

| Primary Insurance | Medicare (Federal Gov.) | Private Plan (Gov.-Contracted Carrier) |

| Doctor/Provider Choice | Any doctor who accepts Medicare (NATIONWIDE) | Must use private network of doctors/specialists (HMO/PPO) |

| Prescription Drug (Part D) | Must purchase separate, stand-alone PDP | Generally bundled in (MA-PD); single ID card for all care |

| Out-of-Pocket Costs | Highly predictable; limited copays/coinsurance depending on plan letter | Less predictable; reliance on copays/coinsurance for services |

| Monthly Premium | Generally higher; separate premium for Medigap + separate Part D | Generally lower combined premium; often a single ID card |

| Extra Benefits (Dental/Vision) | NOT included; separate plan or out-of-pocket for dental, vision | Generally included as dynamic “one-stop-shop” extras |

| Out-of-Pocket Maximum | No government standard max; costs managed by Medigap plan | Mandated government standard out-of-pocket maximum |

The choice is yours, and we are here to help you get started with the precise information you need.

Expert Tips and a Final Checklist for Your Journey

Clarity beats complexity is our standard, but managing the process is where many of us get stuck. Facing this maze together, we can provide precise, expert advice and clear steps. Your enrollment can be joyful, not overwhelming, when you are prepared.

Expert guidance must be detailed content:

- Match Prescriptions First: Never choose a Part D or Medicare Advantage plan without first verifying that your current prescription drugs are on that plan’s formulary and tier structure. This is the single biggest opportunity for cost savings accurate information.

- Understand Your Doctor: Before choosing a Part C plan, always confirm that your trusted doctors and specialists are in that specific private plan’s network, especially if you are opting for an HMO. Do not assume your doctor accepts every private plan.

- Avoid the Late Penalty: Medicare enrollment is a precise life stage, and missing deadlines can be permanent. A detailed checklist will ensure you avoid permanent penalties, especially for Part B.

- Use Free Resources: Utilize free government resources like Medicare.gov’s “Plan Finder” tool, which provides unbiased, cost accurate information accurate information. Contact your State Health Insurance Assistance Program (SHIP) for dynamic, personalized counseling that faces this maze together with you.

Your Final 10-Step Enrollment Checklist

Use this checklist to ensure every step of your journey is structured and joyful.

- [ ] Mark Your Milestone: 65 is your enrollment landmark. Identify your Initial Enrollment Period (IEP)—a precise seven-month window (3 months before, the month of, and 3 months after your 65th birthday).

- [ ] Review Current Coverage: If you are still working, face this maze together with your employer’s health plan. Is it creditable coverage? This is crucial accurate information.

- [ ] Apply for Parts A & B: Generally, you apply through Social Security during your IEP, especially if you are not receiving Social Security yet.

- [ ] Verify Part B Creditable Coverage: If you delay Part B, secure detailed content and written confirmation of your prior creditable coverage.

- [ ] Create Your Comprehensive Medication List: Make this complete. List all your prescriptions and dosages.

- [ ] Check Doctor Networks: Before proceeding, verify all your current providers’ network status.

- [ ] Decide on Your Medicare Path: Choose between Original Medicare + Medigap or a Medicare Advantage plan using Pat & Fran as your guide. Make this complete and joyful.

- [ ] Select Your Specific Plan Letter (Medigap): If you choose Medigap, select your preferred standardized plan (e.g., Plan G or N).

- [ ] Evaluate and Enroll (Part D or Part C): Use Medicare’s “Plan Finder” with your full medication list and doctor information. Compare cost accurate information accurate information.

- [ ] Review annually: Your health care needs change, and plan offerings can change every single life stage. Commit to a yearly 1-hour review during Medicare Open Enrollment to ensure your coverage is always structured for joy.

This process can be structured, dynamic, and purposeful. Facing this maze together, you can find the clarity you need to embrace this major new birthday and your entire senior journey with peace of mind. Let’s get started.