Grit and Gravity: The Reality of Working Past 77

Living in California, I’ve watched the “Golden State” dream create incredible wealth for some, but I’ve also seen it become an unaffordable landscape for many others nearing their senior years. The shimmering promise of a relaxed retirement often collides with the harsh reality of modern economics. Lately, it seems like everywhere I turn, I hear another story that confirms what many of us have quietly feared: the traditional American retirement is under siege.

From volatile stock markets shrinking 401(k) plans to the gut-wrenching sight of seniors facing homelessness, the financial challenges of aging have become impossible to ignore. Tonight, as I reflect on some disturbing trends highlighted by recent reports, I realize that “Retirement Ready” isn’t just a catchy segment title—it is an urgent call to action for every older American. We need to face these truths not with panic, but with grit, grace, and a very practical plan.

By the Numbers: The Chilling Gap Between Hope and Reality

When we look at the benchmarks for a comfortable retirement, the numbers are frankly staggering. The national average suggests a single person needs roughly $967,000 in savings to live out their golden years with ease. That translates to about $74,000 a year—a target that seems entirely reasonable until you look at the actual balances in most retirement accounts.

The typical retirement account balance is just $144,000. And Social Security, which nearly 40% of retirees say is their only source of income, draws an average of only $20,000 a year. If you are relying solely on Social Security, making ends meet isn’t just difficult; it’s often a mathematical impossibility. As one expert starkly put it, “It’s stressful now, but I think we can see the light at the end of the tunnel.” For too many, that light feels like an oncoming train.

The “Sandwich Generation” Squeeze

Adding another layer to this club sandwich of financial pressure is the reality facing many adults in their late 50s and early 60s. We are often part of the “sandwich generation,” simultaneously supporting aging parents and adult children while trying to secure our own futures.

I recently heard the story of Alicia (57) and Chu (59), who are living with three sets of relatives under one roof. When the stock market slides—as the average 401(k) did by 3% recently despite record savings rates—they feel the “motion sickness” of the roller coaster. They don’t have “do-over time.” Their adjusted mindset? Delaying retirement from age 62 or 65 to at least 67. They simply cannot afford a “haircut” on their benefits, and they are not alone. Millions are adjusting their timelines, realizing that work isn’t just something they do; for many, “work is the new retirement.”

The “Work, Retire, Repeat” Syndrome

Perhaps the most troubling trend I’ve observed is what labor economists are calling the “work, retire, repeat” syndrome. Larry (77) and his wife Joyce (66) are living proof. Larry, an electrician by trade, now unloads trailers at a supermarket for $14.75 an hour, leaving home at 5:30 AM. Joyce makes $14 an hour as a legal administrator. “77, still busting my butt,” Larry says. This isn’t the retirement they planned, but with a mortgage, car loan, and other debt, it’s the one they have.

More than half of the people who are currently retired do not have enough money to stay retired. This experiment with the 401(k) as the primary retirement tool—which began 40 years ago as an alternative to traditional pensions—has, for many, failed. Older workers were often never taught enough about saving and investing. As Larry noted, “I grew up on a farm. Nobody there instructed any of us to put money aside and make your own way later.”

The Compounding Challenges: Policy and Staffing Gaps

The financial maze doesn’t end with personal savings. Systemic issues are making it even harder for seniors to access the benefits they earned.

The Social Security Gaps

- Public Sector Inequity: Millions of former public sector employees—teachers, school psychologists like Dee, and police officers—are being shut out of full Social Security benefits due to federal policies like the Windfall Elimination Provision and the Government Pension Offset. For Evelyn (84), working as a cashier, these provisions mean she is denied her husband’s Social Security, costing her an estimated $300,000 over ten years. “This money has been stolen from all of us,” she starkly summarized.

- Wait Time Woes: Even for those who are eligible, getting service is a nightmare. Staffing cuts (12% of jobs eliminated) combined with 13 million new Baby Boomers joining the system have caused average wait times to double in the last six months. Anne, trying to manage care for her brother with dementia, was on hold for six hours. These billionaires making decisions in DC are entirely “out of touch with the real world.”

The Unthinkable Reality: Senior Homelessness

Perhaps most heartbreaking of all is the surge in older Americans experiencing homelessness. On any given night, more than 140,000 people 55 or older are unhoused, a number estimated to nearly triple by 2030. This is the fastest-growing population of the unhoused, uniquely vulnerable not just due to numbers, but because of complex chronic medical conditions (heart disease, diabetes, mental health issues).

The “triggering event” is often the death of a spouse, job loss, or eviction. These are folks prematurely aged by the streets; a 65-year-old unhoused person often physically resembles someone 15 years older. Policy failures in the basic subsistence income programs (like SSI, which pays only $900/month) have left millions destitute. As Rose (65), who navigates asthma treatment by buying used inhalers, said, “I didn’t think it would be like this. It’s just exhausting.”

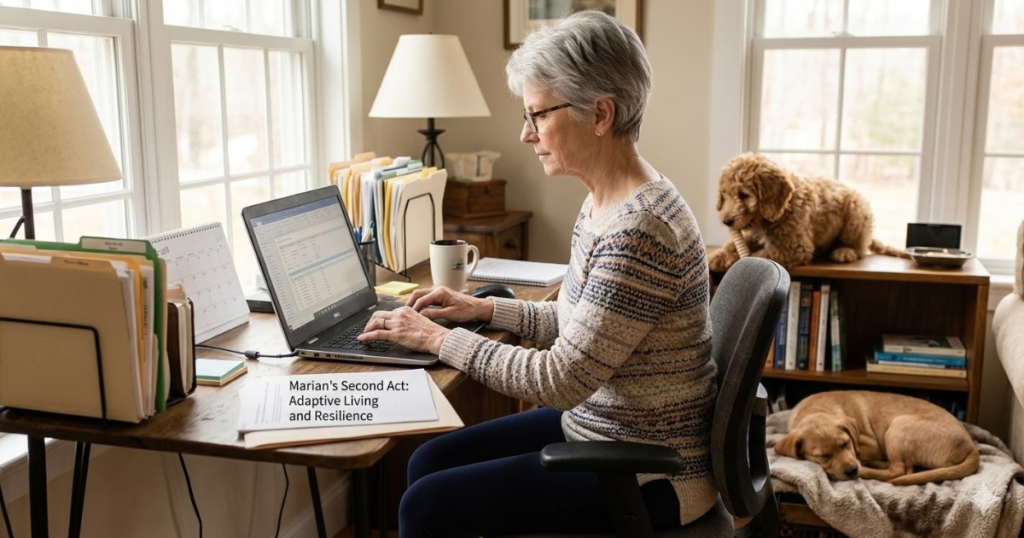

Grace Under Pressure: Marian’s Unplanned Second Act at 66.

Actionable Rules of the Road: Mastering What You Can Control

Despite these formidable challenges, the message must be that it is not too late to make a plan. For those of us without a substantial nest egg, we must embrace the rules of the road physical therapists, financial experts, and determined seniors are practicing. Grit, curiosity, and connection are our new powerful tools.

Rule 1: Master the “When” to Claim Social Security

One of the most powerful moves you can make is deciding exactly when to claim your Social Security benefits. While years sitting—literally—on hold is infuriating, the mathematical reality remains: delaying Social Security benefits until age 70 gets you the largest monthly check possible. This decision can mean thousands of dollars more every year, which is critical for covering rising medical expenses that naturally increase as we age.

Rule 2: Lower Your Cost of Living and Embrace “Live For Now” with Care

If your golden years are tarnished by debt, lowering your cost of living is non-negotiable. Marian (66), facing horribe financial anxiety with no savings and having to work two jobs (sometimes 11 hours a day), had to get creative. She sold her home and co-bought a smaller one with two other women, living together to save money. For her, it was a matter of “life and death.”

If you cannot lower your housing costs, look for other ways to economize. Embrace the “live for now philosophy” not by spending, but by being content with simpler, low-cost options and ensuring every small movement throughout your day reinforcing your grit and stability.

Rule 3: Fund Your Emergency Reserve—But Smartly

Everybody needs a basic plan that starts with connection to their current reality. This means funding an emergency reserve before pushing other goals.

- Still Working? Aim to set aside 6 to 12 months worth of living expenses.

- Already Retired? Make it 1 to 2 years worth.

Crucially, keep that reserve in a safe, easily accessible interest-bearing account. Do not talk to friends or family about this; rely on expert advice. Avoid risky investments promising high returns; the higher the promise, the more you must do in real research to avoid “scarring” that causes detrimental actions during market downturns.

Rule 4: Create Joyful, Purposeful Work (If You Must)

If you must work, look beyond traditional low-wage jobs like Larry’s or Evelyn’s. Marian found a path that was meaningful and sustainable: she formed the trip planning company Kindred Women Travelers, allowing her to see a slice of the world even if she is technically on the job. Find work that connects you to others, utilizes your curiosity, and brings you joy.

Purposeful Planning: Rebuilding Your Financial Foundation with Connection.

A Final Thought on Community and Grace

The journey forward won’t be easy. For Olivia (70), who cannot afford to retire after caring for her husband with MS, the greatest obstacle is simply surviving off Social Security. It is hard for her to accept that she cannot enjoy the rest of her life after working hard all her life. “Just heartbreaking, man.”

But Olivia also found strength. Attending her Bible study group helps her “continue on.” And that is perhaps the most important rule of the road of all. You don’t need to be perfect. Consistency, connection, and care for your body and spirit matter more than perfect financial acumen. Stay strong, stay curious, and lean on your community. We are building a movement, not just budgets, and I am glad you are part of it. Let’s make every step forward a purposeful one.