Navigating the complex landscape of retirement planning can feel overwhelming, especially when you realize that the strategies that served you well during your working years are no longer optimal. As a Baby Boomer, or someone caring for one, you are likely facing the critical pivot point where the focus must shift from accumulating wealth to generating reliable income streams that can sustain a comfortable lifestyle for decades to come.

My journey in financial education has shown me that this transition is rarely straightforward. The sheer volume of choices, coupled with rising costs and complex regulations, often leads to decision fatigue or, worse, costly mistakes. We need to dissect the essential components of a robust Baby Boomer financial strategy, moving beyond generic advice to actionable, deep-dive insights. We will explore how to secure your income, master IRS distribution rules, manage skyrocketing healthcare costs, and establish a legacy that minimizes legal and tax complications.

The decisions made today will define the next twenty, thirty, or even forty years of your life. Let’s explore the strategic framework necessary to master your golden years.

Shifting from Wealth Accumulation to Income Generation

The foundational strategy for Baby Boomers (defined by the U.S. Census Bureau as those born between 1946 and 1964) as they approach or enter retirement is fundamental: you must transition from accumulating wealth to creating a steady flow of income. This is not just about having a large nest egg; it’s about cracking the income code to ensure your savings generate a predictable cash flow that matches your essential and discretionary expenses throughout your golden years.

The accumulation phase was driven by growth and capital appreciation. Now, the priority is distribution and mitigation of risk, specifically longevity risk—the very real danger of outliving your savings.

The Role of Annuities as Guaranteed Income

One highly effective strategy to mitigate longevity risk is to convert a portion of your retirement savings into an annuity. Annuities are financial contracts, typically with insurance companies, that provide a stream of payments for a specified period, or, crucially, for the remainder of your life. By allocating a specific percentage of your assets to an annuity, you are creating your own “personal pension,” a source of income that is guaranteed, predictable, and immune to market volatility.

This strategy is particularly beneficial for covering core, essential expenses (housing, utilities, food). A guaranteed cash flow provides the baseline security needed to enjoy retirement without constant anxiety about market downturns decimating your principal.

Leveraging Dividend-Paying Stocks for Growth and Income

Another core strategy involves investing in a diversified portfolio of dividend-paying stocks. These equities offer a powerful dual advantage that annuities cannot: they provide regular income through quarterly dividend payments, while also offering the potential for capital appreciation (the stock price increasing).

This combination makes dividend stocks an exceptional tool for countering inflation—the slow, subtle erosion of your purchasing power over time. A portfolio that focuses on “dividend aristocrats”—companies with a long history of raising their dividend payouts every year—can generate an income stream that grows over time, helping to ensure your lifestyle doesn’t shrink as costs rise. It’s critical, however, to diversify these holdings across different sectors to reduce the risk associated with any single company or industry. Consulting with a financial advisor is crucial here to tailor your allocation to your personal risk tolerance.

Navigating the RMD (Required Minimum Distribution) Requirements

A major pitfall for many retirees lies within the precise and often complex rules governing Required Minimum Distributions (RMDs). For decades, you likely maximized tax-deferred retirement accounts, such as traditional IRAs, 401(k)s, and 403(b)s, taking advantage of upfront tax breaks. The trade-off is that Uncle Sam will eventually demand his share of that money.

Once you reach a certain age, the IRS forces you to withdraw a minimum amount annually. As of the passing of SECURE 2.0 (2023), the beginning age for RMDs is 73.

The specific RMD amount is not static; it is calculated using a dynamic formula that considers both your account balance (at the end of the previous calendar year) and your life expectancy, as determined by IRS Uniform Lifetime Tables.

The 25% Penalty for Non-Compliance

It is absolutely essential to understand that failing to make these required distributions accurately and on time can result in severe financial penalties. If an RMD is not withdrawn by the deadline (generally December 31st of each year, with specific nuances for the first RMD), you might face an excise tax penalty of up to 25% of the amount that should have been withdrawn.

For instance, if you were required to withdraw $10,000 and failed to do so, you could owe a penalty of $2,500. While this penalty can sometimes be reduced to 10% if the mistake is corrected in a timely manner (often called “reasonable cause”), the best strategy is proactive compliance. Avoiding this trap requires careful planning, deep understanding of the rules, and integration of RMDs into your broader retirement income strategy to optimize your tax liabilities.

The Healthcare Challenge: Budgeting for the Unavoidable

Rising medical costs are a relentless reality in retirement planning, often becoming one of the most significant and unpredictable expenses a retiree faces. Longer life expectancies mean we are managing chronic conditions and healthcare needs for a greater number of years. Effective planning must account for both routine care (prescriptions, check-ups) and the potential for unexpected major medical events, such as a severe illness or injury.

The Critical Distinction: Medicare and Long-Term Care

Planning starts with Medicare, the federal health insurance program for people 65 or older. While essential, Medicare is rarely all-encompassing. You must understand the different components (Part A, Part B, Part C/Medicare Advantage, Part D for prescriptions) and what each part covers versus what it excludes.

Crucially, Medicare and Medigap (Medicare Supplement) policies generally do not cover most costs associated with long-term care (LTC). This includes extended services like assisted living facility costs, nursing home care, or in-home health aides to manage daily activities—all of which are astronomically expensive. For many, a dedicated long-term care insurance policy is a necessary layer of protection against these catastrophic costs.

Beyond insurance, you should build a dedicated healthcare contingency fund. If you were eligible, maximizing contributions to a Health Savings Account (HSA) during your working years provides a powerful, tax-advantaged vehicle for retirement medical expenses, as HSA funds can be withdrawn tax-free for qualified medical costs.

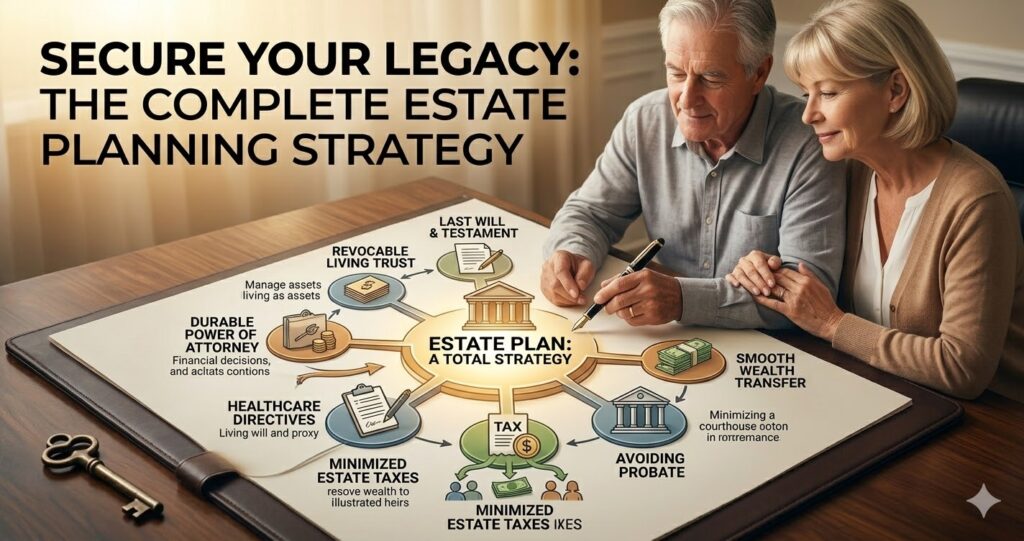

Beyond the Will: The Complete Estate Planning Strategy

A vital, but frequently deferred, final step is comprehensive estate planning. This goes far beyond simply drafting a Will. While a Will is a starting point, it only dictates how assets passing through probate are distributed.

A complete estate plan is a holistic, multi-faceted strategy designed to achieve several critical objectives:

- Ensuring asset distribution: Making sure your assets pass smoothly to your desired beneficiaries according to your exact wishes.

- Minimizing Taxes and Costs: Implementing legal structures to reduce the burden of estate taxes (which, though high, apply to few) and income taxes for your heirs.

- Avoiding Probate: Crafting a plan that minimizes or entirely skips probate, which is a potentially lengthy, public, and expensive court-supervised legal process.

- Planning for Incapacity: Providing clear legal mechanisms to manage your personal and financial affairs if you ever become unable to make decisions for yourself during your lifetime.

The Crucial Tools: Trusts, POA, and Directives

Achieving these goals requires a sophisticated array of legal tools and documents that work together:

- Trusts: Living trusts (revocable) can bypass probate entirely, maintaining privacy and distributing assets efficiently. Irrevocable trusts can be used to minimize estate taxes and protect assets from creditors or long-term care costs.

- Power of Attorney (POA): Designates a trusted individual (your ‘agent’) to manage your financial matters if you are incapacitated.

- Healthcare Directives (Living Will and Healthcare Proxy): Clearly outlines your medical wishes for end-of-life care and designates a person to make medical decisions on your behalf when you cannot.

- Beneficiary Designations: Ensuring your life insurance, retirement accounts, and “Transfer on Death” (TOD) or “Pay on Death” (POD) bank accounts have correctly designated beneficiaries, as these assets pass outside of probate by contract.

Regularly reviewing and updating these documents is as important as creating them. Consulting with a qualified estate planning attorney is essential to ensuring your specific strategy minimizes taxes, prevents family conflict, and provides you with the ultimate peace of mind.

Conclusion and Final Check

We have covered significant terrain, from generating income that counteracts longevity risk to mastering the IRS’s distribution rules, preparing for the rising costs of healthcare, and designing a comprehensive estate plan that preserves your legacy. This journey, I’m Kathy, and I’m grateful to be a part of yours toward financial empowerment.

I would like to wrap up this guide with the three questions mentioned in the introduction:

- Why might dividend stocks be helpful to you in retirement? They offer the potential for both regular income (quarterly payouts) and capital appreciation (price growth), making them a vital tool to help your income outpace inflation.

- Why do you need more than just a Will? A Will only manages assets passing through probate. Comprehensive planning needs trusts (to avoid probate and manage privacy/taxes), Power of Attorney (for financial incapacity), Healthcare Directives (for medical wishes), and correct beneficiary designations to ensure a smooth, complete, and low-conflict transfer of your legacy.

- At what age do you need to start taking your RMDs as of 2023? Once you reach age 73.

I am dedicated to helping you build confidence in your relationship with money. Please let me know in the comments below which topics you would like to see covered in a deep-dive analysis. If you are new to the SeniorJourneyBlog community, please subscribe—it truly helps support the creation of this detailed financial content, so that you too can take control of your financial journey.

🌿 Weekly wellness, health & beauty insights — straight to your inbox

Free subscription · Cancel anytime