Medicare Advantage vs. Original Medicare in 2026: Which Is Better for You Now?

By the SeniorJourney Editorial Team | Updated May 2026 | 8-min read

Let me tell you about a conversation I had with my neighbor Dorothy — a sharp, energetic 68-year-old who spent three weeks last fall going through every Medicare brochure she could find, spreading them across her kitchen table like a jigsaw puzzle she was determined to solve. “I just want someone to tell me the truth,” she told me. “Not the sales pitch. The truth.”

If you’ve ever felt like Dorothy, you’re not alone. Every year, millions of Americans over 65 face one of the most consequential decisions of their retirement: Original Medicare or Medicare Advantage? And in 2026, the stakes are higher than ever — premium costs have shifted, benefit structures have changed, and a new wave of plan options has flooded the market.

This guide cuts through the noise. We’ll walk you through the real differences, share what actual beneficiaries are experiencing, and give you a practical action plan to find the plan that fits your life — not someone else’s brochure.

Cost comparison: Original Medicare vs. Medicare Advantage in 2026

Understanding the Basics: What Are These Two Programs?

Before we dive into the comparisons, let’s get grounded. Original Medicare is the federal government’s traditional health insurance program, made up of two core parts:

- Part A — Hospital insurance: covers inpatient hospital stays, skilled nursing facility care, hospice, and some home health services.

- Part B — Medical insurance: covers doctor visits, outpatient procedures, preventive services, and durable medical equipment.

Medicare Advantage (Part C), on the other hand, is a privatized alternative offered through insurance companies approved by Medicare. These plans bundle Part A and Part B coverage — and usually Part D (prescription drugs) — into a single plan, often with extra perks like dental, vision, and hearing coverage.

Think of it this way: Original Medicare is the classic, time-tested framework. Medicare Advantage is a packaged deal — potentially more convenient, but with its own set of rules and restrictions.

Sponsored

😴 Waking Up Stiff and Restless? Your Body May Need More Magnesium.

As we age, magnesium levels naturally decline — and most of us don’t even know it. Doctor’s Best High Absorption Magnesium uses patented TRAACS® chelate technology for up to 6x better absorption than standard supplements. Gentle on digestion, vegan, and non-GMO. Trusted by seniors for over 35 years.

Shop Doctor’s Best Magnesium on iHerb →*These statements have not been evaluated by the FDA. Not intended to diagnose, treat, cure, or prevent any disease.

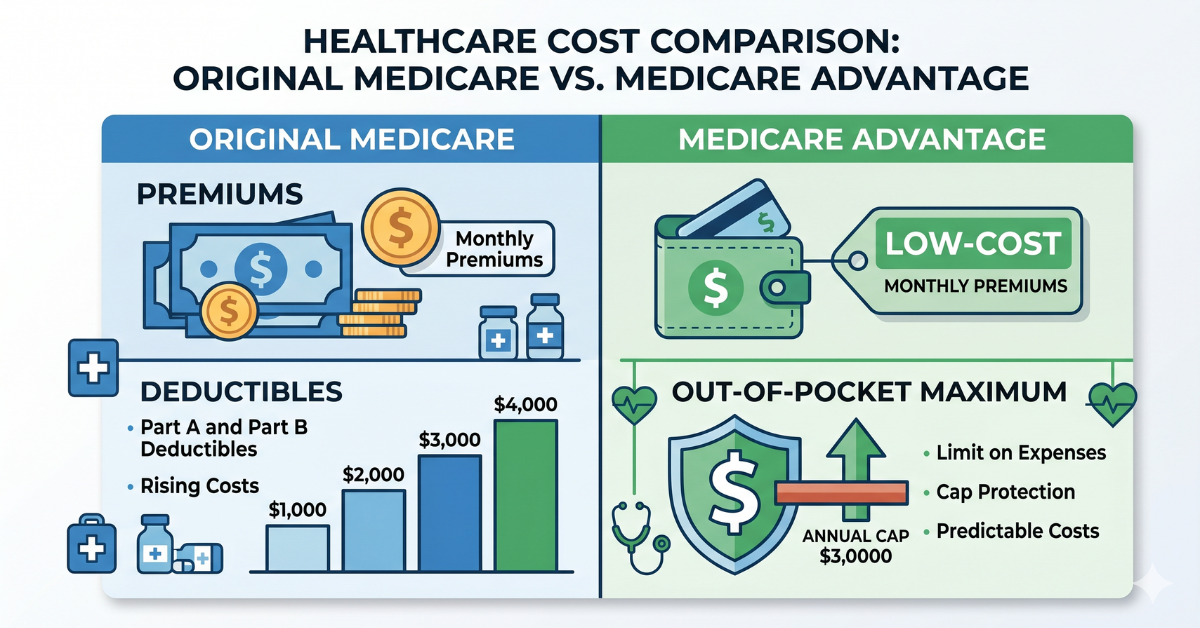

The Real Cost Difference in 2026: What Will You Actually Pay?

Money matters — and this is where most people get tripped up. The costs of Medicare are more layered than a simple monthly premium, and in 2026, there are some important updates to be aware of.

Original Medicare Costs

With Original Medicare, you pay the Part B standard monthly premium (estimated at approximately $185/month for most enrollees in 2026). On top of that, you pay a 20% coinsurance on most Part B services — with no cap on how much that can add up to. A serious illness, major surgery, or extended hospital stay can result in thousands of dollars in out-of-pocket costs.

That’s why many Original Medicare enrollees also purchase a Medigap (supplemental) policy to help cover those gaps. These plans typically run anywhere from $100 to $300+ per month depending on your age, location, and the level of coverage you choose.

Medicare Advantage Costs

Many Medicare Advantage plans advertise $0 additional monthly premiums beyond your Part B payment — a feature that understandably turns heads. But here’s the important context: these plans make their money through network restrictions, prior authorization requirements, and cost-sharing structures that kick in when you use services.

The key advantage of Part C plans is the mandatory annual out-of-pocket maximum — set by CMS, this cap in 2026 is roughly $8,850 for in-network services. Once you hit that number, the plan pays 100% for the rest of the year. This is real financial protection that Original Medicare simply doesn’t offer on its own.

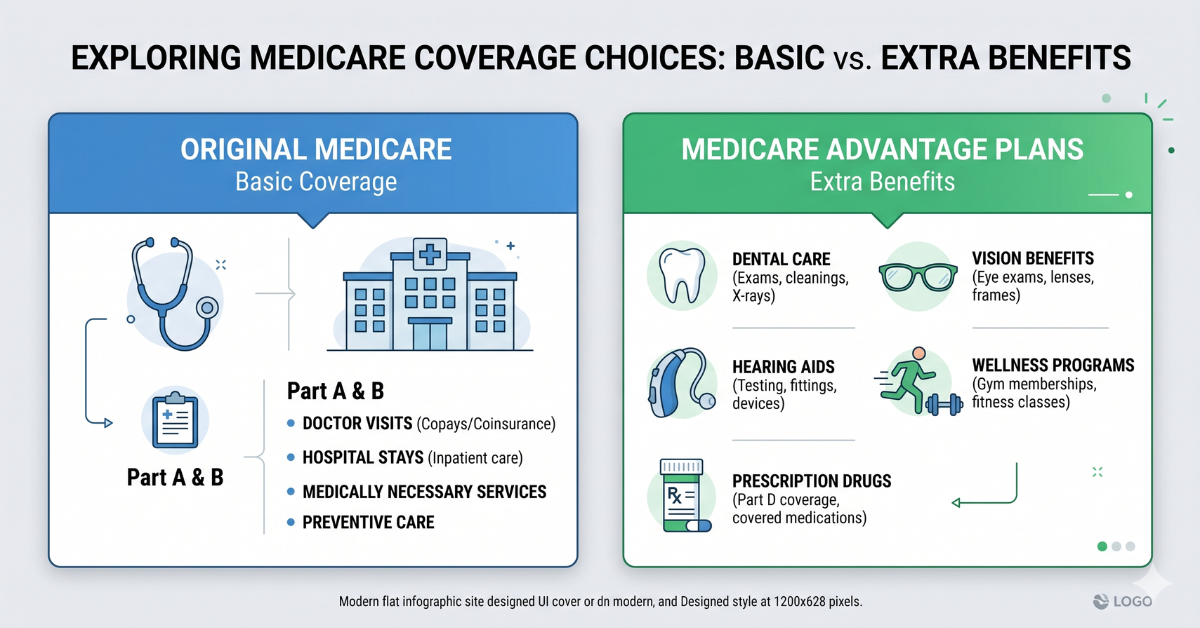

Coverage & benefits: what’s included in each plan type

Benefits Beyond the Basics: Where Medicare Advantage Shines

One of the most frequently cited reasons seniors choose Medicare Advantage is the roster of extra benefits that Original Medicare doesn’t cover. In 2026, many Part C plans include:

- Dental coverage — including routine cleanings, X-rays, and in some cases, dentures or implants

- Vision benefits — annual eye exams, prescription glasses or contact lens allowances

- Hearing aid coverage — a genuinely transformative benefit for the millions of seniors with hearing loss

- Fitness memberships — programs like SilverSneakers® or similar gym access benefits

- Transportation to medical appointments — a lifeline for those who no longer drive

- Meal delivery after hospitalization — available through some plans post-discharge

Dorothy — the neighbor I mentioned at the start — ultimately chose a Medicare Advantage plan largely because of the dental and vision benefits. “I was spending over $800 a year out of pocket on my teeth,” she told me after her first year on the plan. “The Advantage plan covered most of that. For me, it was a no-brainer.”

That said, benefits vary enormously from plan to plan and county to county. Always verify what a specific plan covers in your zip code before enrolling.

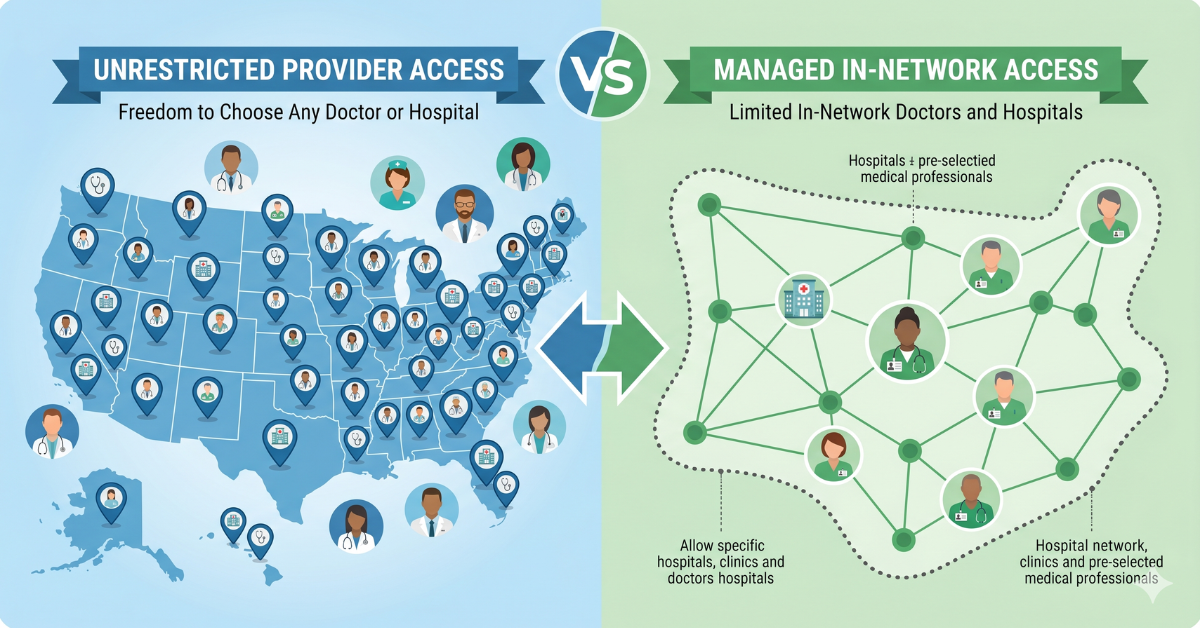

Doctor & hospital choice: how each plan affects your access

Doctor & Hospital Choice: The Freedom Factor

For many seniors, the ability to choose their own doctors is non-negotiable. This is one of the most significant practical differences between the two programs.

With Original Medicare, you can see any doctor, specialist, or hospital in the country that accepts Medicare — and most do. There are no referrals required, no network restrictions, and no prior authorizations for most services. If you split time between Florida and Minnesota, or if you have a specialist relationship you’ve built over decades, Original Medicare gives you total freedom.

With Medicare Advantage, most plans operate as HMOs (Health Maintenance Organizations) or PPOs (Preferred Provider Organizations). HMOs typically require you to stay within a defined network of providers and get a referral before seeing a specialist. PPO plans offer more flexibility but usually still charge more for out-of-network care.

My own father learned this the hard way. He switched to a Medicare Advantage HMO to save money on premiums, only to discover that his longtime cardiologist wasn’t in-network. The process of getting a new cardiologist, getting the referrals in order, and navigating prior authorization for a procedure he needed took over six weeks. “I felt like I was fighting the system,” he said, “right when I needed it most.”

If provider continuity and freedom of access are top priorities for you — especially if you manage a complex chronic condition — this difference deserves very serious weight.

Sponsored

❤️ Your Heart Works Hard Every Day. Give It the Support It Deserves.

California Gold Nutrition Omega-3 Premium Fish Oil delivers 360mg EPA + 240mg DHA per serving in fish gelatin softgels — porcine and bovine free, molecularly distilled for purity, and manufactured in California. Thousands of users over 50 report improvements in heart health, cholesterol levels, joint comfort, and even hair health.

“As someone in my 50s, I’ve noticed a significant benefit in my heart health and reduced inflammation. My cholesterol levels have improved.” — Verified iHerb Reviewer

Shop Omega-3 Fish Oil on iHerb →*These statements have not been evaluated by the FDA. Not intended to diagnose, treat, cure, or prevent any disease.

Prescription Drug Coverage: Don’t Overlook Part D

Prescription medications are often one of the largest healthcare expenses for seniors. Here’s how the two paths handle it:

With Original Medicare, prescription drug coverage is not included. You must enroll in a separate Part D plan to cover your medications. If you don’t enroll when first eligible and go without creditable coverage, you’ll face a late enrollment penalty that permanently increases your Part D premiums.

Most Medicare Advantage plans bundle Part D coverage right in, which simplifies things considerably. One card, one plan, one set of rules. However, you need to verify that your specific medications are on the plan’s formulary (approved drug list) and check the tier-based cost-sharing structure carefully.

A major development for 2026: thanks to the Inflation Reduction Act provisions continuing to take effect, Medicare Part D out-of-pocket drug costs are now capped at $2,000 annually — a landmark protection for seniors on expensive medications. This cap applies whether you’re on a standalone Part D plan or a Medicare Advantage plan with drug coverage.

✅ Your 2026 Medicare Decision: A Step-by-Step Action Plan

Don’t just read about it — act on it. Here’s a practical, proven process to help you make the right choice:

Step 1: List Your Current Doctors and Medications

Before comparing plans, write down every doctor you see regularly — primary care, specialists, and any hospital you’ve used. Also list every prescription medication you take, along with dosage. This is your personal checklist. Any plan you seriously consider must cover your doctors (if it’s a network plan) and your medications at an acceptable cost tier.

Step 2: Use Medicare’s Official Plan Finder Tool

Go to Medicare.gov/plan-compare and enter your zip code. The tool will show you all available plans in your area — both Part D standalone plans and Medicare Advantage plans — along with estimated annual costs based on your specific medications. This is the most powerful free tool available to you, and most seniors don’t use it to its full potential.

Step 3: Call Your State SHIP Counselor for Free, Unbiased Help

Every state has a free State Health Insurance Assistance Program (SHIP). These trained counselors have no financial stake in which plan you choose — unlike insurance agents, who earn commissions. They can walk you through your specific situation, review plan details with you, and help you understand enrollment deadlines. Call 1-800-MEDICARE to be connected to your local SHIP.

Step 4: Revisit Your Decision Every Year During Open Enrollment

Medicare’s Annual Enrollment Period (AEP) runs from October 15 to December 7 each year. Plans change their benefits, premiums, formularies, and networks annually — meaning the best plan for you last year may not be the best plan for you now. Make it a yearly habit to compare your current plan against alternatives, even if you ultimately stay put.

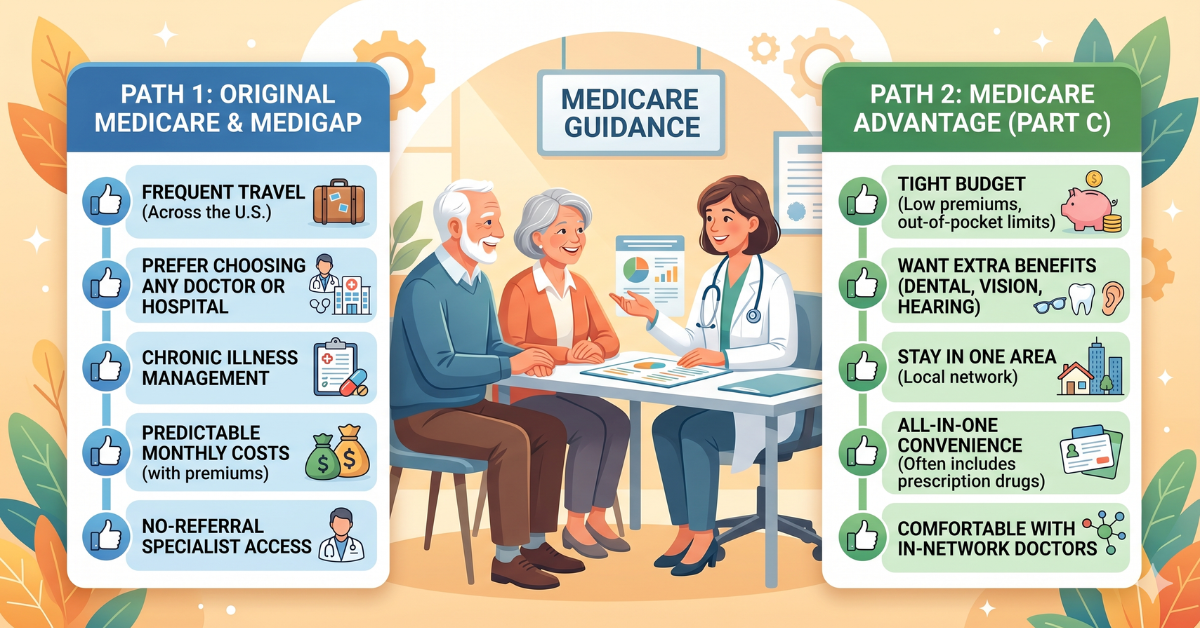

Finding the right Medicare plan for your life in 2026

Who Should Choose Original Medicare in 2026?

Original Medicare paired with a Medigap plan tends to be the stronger choice if you:

- Travel frequently across the U.S. or spend time in multiple states

- Have established relationships with specific specialists you don’t want to lose

- Are managing a complex chronic condition that requires frequent specialist visits

- Live in a rural area where Medicare Advantage networks may be limited

- Value predictable costs above all else and can afford Medigap premiums

Who Should Choose Medicare Advantage in 2026?

Medicare Advantage tends to be the stronger choice if you:

- Want to minimize monthly premium costs (especially on a fixed income)

- Need dental, vision, or hearing coverage that Original Medicare doesn’t provide

- Live in an urban or suburban area with a robust, well-rated plan network

- Are generally healthy and don’t anticipate extensive specialist use

- Want the convenience of an all-in-one plan with built-in Part D coverage

Sponsored

🦠 A Healthy Gut Is the Foundation of a Healthy Senior Life

As we age, our gut microbiome naturally weakens — affecting digestion, immunity, and even mood. California Gold Nutrition LactoBif® 30 Probiotics delivers 30 Billion CFU across 8 carefully selected strains (5 Lactobacilli + 3 Bifidobacteria) in individually double-foil blister-sealed capsules. No refrigeration needed. No fishy aftertaste. Just daily digestive balance you can feel.

“Lactobif is an excellent probiotic. I took it for a long time, and my gut felt great and balanced the whole time.” — Verified iHerb Reviewer

Shop LactoBif Probiotics on iHerb →*These statements have not been evaluated by the FDA. Not intended to diagnose, treat, cure, or prevent any disease.

The Bottom Line: There’s No Single “Best” Plan — But There Is a Best Plan for You

After years of watching this decision play out for people I care about — and studying the landscape carefully as a retirement planning professional — I can tell you with confidence: the question isn’t which plan is objectively better. The question is which plan fits your health profile, your budget, your travel habits, your doctor relationships, and your peace of mind.

Dorothy went with Medicare Advantage and has been thrilled. My father, after his experience with network restrictions, switched back to Original Medicare with a Medigap plan and says it was the best decision he ever made. They’re both right — for their own situations.

Take the time. Use the tools. Talk to a SHIP counselor. And revisit this every year. Your health — and your financial security — are worth the effort.

📺 Want to See This Explained Step by Step on Video?

Head over to our YouTube channel SeoulcastUSA — we’ve put together easy, friendly video guides walking you through Medicare decisions, retirement planning, and senior health tips. No jargon. No pressure. Just honest, practical guidance for the journey ahead.

Visit SeoulcastUSA on YouTube →Health & Financial Disclaimer: The information in this article is for educational purposes only and does not constitute medical or financial advice. Medicare plan details, premiums, and benefits are subject to change annually. Always consult a licensed Medicare advisor, your physician, or your State SHIP counselor before making enrollment decisions. Supplement information is not intended to diagnose, treat, cure, or prevent any disease. These statements have not been evaluated by the Food and Drug Administration.

💡 Frequently Asked Questions (FAQ)

Can I switch from Medicare Advantage back to Original Medicare?

Yes. You can switch during the Annual Enrollment Period (October 15–December 7) each year. You can also switch back during the Medicare Advantage Open Enrollment Period (January 1–March 31), which allows you to move from a Medicare Advantage plan to Original Medicare and join a standalone Part D drug plan. However, if you want to buy a Medigap policy after switching back, you may face medical underwriting in most states — meaning insurers can charge more or deny coverage based on your health history.

Does Medicare Advantage cover care when I travel outside my plan’s service area?

Most Medicare Advantage plans cover emergency and urgently needed care anywhere in the United States, even outside your plan’s network. However, routine care — regular doctor visits, specialist appointments, elective procedures — typically must be obtained within your plan’s service area and network. For frequent travelers or “snowbirds” who split time between states, Original Medicare is almost always the more practical choice.

What is the Medicare Part D out-of-pocket drug cost cap in 2026?

Thanks to the Inflation Reduction Act, the annual out-of-pocket cap for Medicare Part D prescription drug costs is $2,000 in 2026. This applies to both standalone Part D plans and Medicare Advantage plans that include drug coverage. Once you’ve spent $2,000 on covered drugs in a calendar year, your plan pays 100% for the remainder of the year. This is a landmark protection for seniors on high-cost medications.

Is it true that Medicare Advantage plans can be taken away or changed?

Yes, this is a real concern. Medicare Advantage plans are offered by private insurance companies that can change their benefits, premiums, cost-sharing, and provider networks each year — or even exit your market entirely. If your plan exits, you’ll receive a Special Enrollment Period to choose a new plan. This uncertainty is one reason some seniors prefer the stability of Original Medicare, which is a federal program with more consistent rules.

Where can I get free, unbiased help comparing Medicare plans?

The best free resource is your state’s State Health Insurance Assistance Program (SHIP). SHIP counselors are federally funded volunteers with no commission motive — they exist solely to help you understand your options. You can reach them by calling 1-800-MEDICARE (1-800-633-4227). You can also use the official Medicare Plan Finder at Medicare.gov/plan-compare to compare plans in your zip code based on your own medications and doctors.

🌿 Weekly wellness, health & beauty insights — straight to your inbox

Free subscription · Cancel anytime

")