When January arrives, most of us receiving Social Security look forward to that friendly notification detailing our annual Cost-of-Living Adjustment (COLA). It’s a moment of optimism, promising a little more breathing room in our monthly budgets. We’ve seen significant fluctuations in these adjustments over the past decade, driven entirely by inflation. They ranged from a minimal 0.3% increase in 2017 to the substantial, historic hike of 8.7% in 2023. For 2026, we saw a COLA of 2.8%.

Understandably, when those checks go up, everyone is pleased. But I have sat across the desk from many clients who received the exact opposite: a notice that their Social Security check was decreasing. This can be a very surprising and disappointing blow to your financial plan. Throughout my career helping seniors navigate retirement finance, I’ve learned that a decrease is rarely a permanent penalty, but rather the result of specific interactions between your income, your health coverage, and Social Security’s complex rulebook.

A decrease isn’t an arbitrary punishment. It is almost always a recovery of money the system believes it overpaid you, or a payment for other services you are receiving. It is critical to understand why this happens and, just as importantly, what you can do about it. In this guide, I’m going to detail the six specific reasons why your Social Security check can be decreased and provide actionable steps to correct or prepare for these reductions.

The Impact of Working: The Social Security Earnings Test

The first and arguably most common reason for a sudden decrease in benefits is the Social Security Earnings Test. If you choose to continue working and earning wages while also collecting Social Security benefits before you reach your Full Retirement Age (FRA), your check is subject to significant reductions. It is a common misconception that once you qualify, you can collect the full amount regardless of work. This is not true.

The key distinction here is that we are talking about earned income—specifically wages or net earnings from self-employment. Investment income, pensions, annuities, and rental property income (unless you are a real estate professional) do not count toward the earnings test.

The earnings test applies only until you hit your FRA. Let’s look at a scenario I’ve seen play out frequently, using a specific birthdate to show the strict timelines involved. If you were born on July 4, 1960, your Full Retirement Age (anyone born in 1960 or later) is 67. Therefore, this person’s FRA would be July 1, 2027. From that date forward, they have no earnings test whatsoever and can make unlimited income.

However, prior to that date, two levels of the test apply: a low amount for most years, and a high amount for the specific year you reach FRA.

High vs Low Limits

We have different limits set annually. In my example, our subject could take reduced benefits as early as 62, starting July 1, 2022. During these early years, the low limit applies. In 2026, the low earnings test amount is $24,480 annually. That is all this individual can earn without penalty between July 1, 2022, and December 31, 2026 (the year before their FRA).

Let’s see the financial consequence. If this person makes exactly $12,000 above that $24,480 limit, Social Security imposes a penalty. For every $2 you are above the limit, they take $1 out of your check. If their monthly benefit is $2,000 (roughly average), making $12,000 over results in a full $6,000 penalty.

Social Security recovers this penalty by withholding your entire monthly check. They don’t just reduce your $2,000 check by $500 for twelve months. In this example, they would withhold three consecutive checks ($2,000 * 3 = $6,000) for January, February, and March. Your social security check drops all the way to zero. Only after the full penalty is recovered (starting in April) would your $2,000 payments resume.

A special high earnings test applies in the actual year you reach FRA. For our July 4th, 1960 born subject, this high amount would cover the months of January 2027 through June 2027. The high limit for 2026 is $65,160, and the penalty is substantially less: they only take $1 for every $3 you earn over that high limit. If they made $12,000 above the $65,160, the penalty is $4,000. They would only withhold two months of checks ($2,000 * 2) instead of three.

Expert Tip: Many people choose to work part-time in retirement. If you are under FRA, track your income month by month. The Social Security Administration does not get these records from your employer for 6 to 12 months. It is your responsibility to report your estimated earnings to avoid a shock recovery later.

“Once I hit full retirement age, I can make as much as I want. There’s no effect to my social security check at all.”

When Social Security Says You Owe: Overpayment Recovery

The second reason I see frequently in my career is Overpayment Recovery. This occurs when Social Security reviews its records and determines it paid you too much. While this can happen due to administrative error (which I will touch on), it is almost always triggered by failures to report information that would have reduced your benefit.

There are four main issues leading to this situation:

- Unreported Earnings (Before FRA): As just discussed, if you are under FRA and work but fail to notify Social Security of your income, you will be subject to a penalty recovery months later once tax records are processed.

- Change in Income (Failure to Update Estimate): Similar to above, this applies if you provide an estimated income (say, $20,000) that is just below the limit, but you get a raise, a new job, or pick up extra shifts and actually earn above the limit. Your benefits should have gone down, but didn’t because you didn’t report that life-changing event.

- Social Security Administration Error: Sadly, this does happen. SSA makes clerical mistakes, updates records slowly, or experiences a delay in getting information. They may have been aware of your income change, but continued paying the incorrect, higher amount anyway. When they finally catch the error, you are still responsible for repaying that “windfall.”

- Disability Review Overpayments: For people on SSDI (disability), you are permitted to work, but you cannot engage in “Substantial Gainful Activity” (SGA), which is earning above specific monthly limits. Reviews are intermittent, and it often takes a few months to catch SGA violations. Once caught, Social Security may backdate the termination of benefits, making all checks received since that review date an “overpayment.”

When any of these four overpayment scenarios occur, your check will definitely decrease until the money is recovered.

Your Recovery Options:

It is crucial to understand that a decrease is not fraud, nor is it intended to punish you. Social Security views it as balancing the books.

- hardship Plan: You have the right to request a waiver if paying it back causes significant financial hardship.

- Payment Plan: If you cannot afford the immediate recovery (losing several full checks), you can almost always set up a monthly payment plan.

- Right to Appeal: You also may request a waiver and actually appeal this if you don’t think it’s right. If you have documentation proving they were notified, appeal immediately.

The Medicare Connection: Automatic Premium Deductions

The third major factor that causes Social Security checks to decrease is Medicare premiums. This is often the biggest shock for those who take Social Security “early” (before 65) and then age into Medicare.

Let’s use an example of a senior whose birthday is October 15, 1961. This person took early Social Security at 62 (October 1, 2023) and has been happily receiving that check. They are automatically eligible for Medicare A and B on the first day of the month they turn 65, which is October 1, 2026. This is their Medicare effective date.

A crucial point I must emphasize: If you are already taking Social Security benefits when you turn 65, you will be automatically enrolled into Medicare Parts A and B. Nothing you can do; it’s going to happen.

The Medicare card arrives automatically right before your 7-month initial enrollment period (IEP) window begins. In our example, the IEP is July 2026 through January 2027. This person will get their card in the mail, enrolling them in A and B, around June 15 or 20, 2026.

Here is the financial decrease: If they keep the card and begin Medicare on October 1, 2026, their next Social Security check (received that same month) will go down. Everyone on Medicare pays the Part B premium. In 2026, the standard Part B premium is $202.90 per month.

If you are not on Social Security, Medicare bills you for this premium quarterly or allows for automatic bank draft. But if you are on Social Security, it has to come out. This means that check you receive during the first month of Medicare is guaranteed to be less exactly $202.90.

Furthermore, some seniors also choose to have their Medicare Part D (prescription drug) plan premium deducted directly. I have a drug plan that costs $9.60 a month; adding that deduction would cause your check to decrease further, by a total of $212.50.

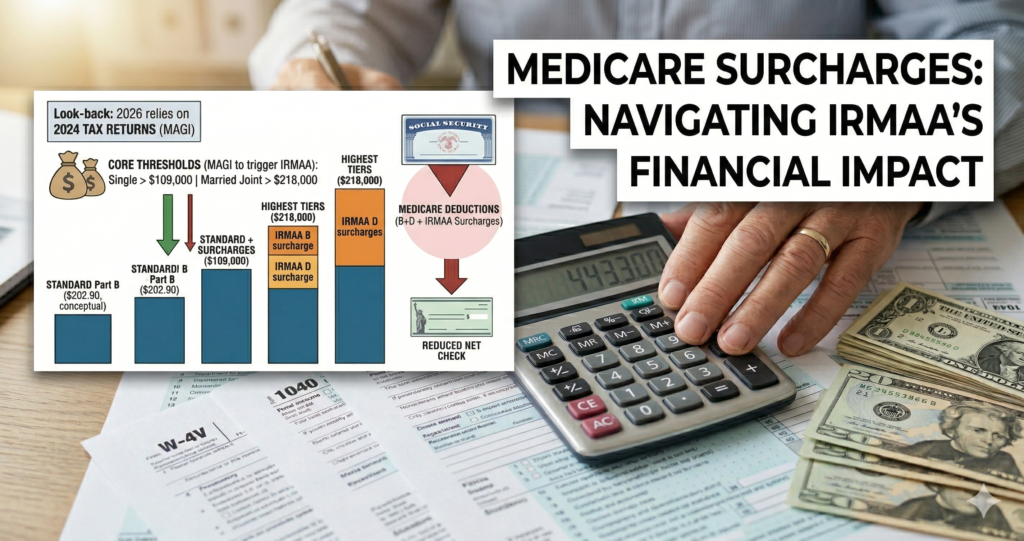

High Earners Beware: IRMAA Surcharges Explained

While the standard Part B premium ($202.90 in 2026) affects the majority, reason number four is a specific surcharge for those deemed to be “high income.” This is called IRMAA, an acronym standing for Income-Related Monthly Adjustment Amount.

IRMAA is a progressive surcharge added on top of both the standard Part B premium and the Part D drug premium. About 85% of the population does not have to worry about IRMAA, but it can make your Social Security checks decrease drastically if you are a higher earner.

IRMAA is calculated based on your Modified Adjusted Gross Income (MAGI). This formula is specific: you must look at your tax return from two years prior and take your AGI (Line 11) plus your tax-exempt interest (Line 2a). That combined figure is your MAGI.

Social Security sets strict income thresholds annually. If your MAGI stays below these, you pay only the standard Part B premium. If you go above them, you trigger IRMAA for both B and D.

Navigating IRMAA Thresholds

I have seen many seniors stunned by an IRMAA notice because they are looking at their current retirement income (maybe only pensions and Social Security) rather than their tax returns from two years ago.

For 2026, Social Security looks back to your 2024 tax return (MAGI) to set your 2026 premium. The core thresholds that trigger IRMAA in 2026 are:

- Single Filer: $109,000 (MAGI from 2024 tax return).

- Married Filing Jointly: $218,000 (MAGI from 2024 tax return).

If you made even one dollar over $109k or $218k in 2024, you trigger the first surcharge tier.

To illustrate, let’s assume a married couple filing a joint return with a 2024 MAGI between $274,000 and $342,000. They have triggered IRMAA for both Part B and Part D.

Their monthly premiums deducted from Social Security would be:

- Standard B: $202.90

- Irmaa B Surcharge: $202.90

- Part D Premium (Plan Cost): $9.60

- Irmaa D Surcharge: $37.50

Total deducted monthly from one Social Security check: $443.30.

If you are on Social Security, these IRMAA surcharges must be deducted from your check. This will result in a drastic and very frustrating reduction.

“High income and Medicare surcharges: if you are on social security, that social security check is going to be drastically reduced.”

Appealing IRMAA (Form SSA-44)

Do not assume you are automatically stuck with IRMAA. You have the right to request an IRMAA reconsideration or appeal. If you had IRMAA in 2026 because they looked at 2024, but you retired in 2025 (a life-changing event) and your 2025 or 2026 income will be drastically lower, you can fight it.

The primary, most common reasons (out of eight possible life-changing events) to appeal IRMAA include:

- Work Stoppage: (Totally retired).

- Work Reduction: (Semi-retired).

- Marriage, Divorce, or Death of a Spouse.

I have done many appeals for clients using these reasons. There are also three other unique situations: 4. Loss of Income-Producing Property: (e.g., a flood, mudslide, or fire destroyed a rental duplex). This is not selling property at a loss. 5. Loss of Pension Income. 6. Employer Settlement Payment.

When you appeal using Form SSA-44, you provide Social Security with the specific date of the life-changing event and your new projected MAGI numbers. You can project for 2025 or 2026. As long as you stay below the core threshold ($109k or $218k), your IRMAA surcharges will drop off entirely.

Action Plan: If you receive an IRMAA notice and have had one of these events, appeal it as soon as possible. Do not wait.

Choosing to Pay Now: Voluntary Tax Withholding (Form W4V)

The fifth reason your check could decrease is actually income taxes, and this one is unique because it is voluntary. You purposely asked them to make this deduction.

I think most of you know that none of us would have to pay taxes on 100% of our Social Security income, but some seniors could pay a substantial amount if they are in higher tax brackets. To avoid having to make quarterly estimated tax payments or having a large tax bill at the end of the year, many seniors find it easier to simply have the taxes withheld directly.

To determine how much of your Social Security is taxable, we look at the provisional income formula. This uses AGI (Line 11), plus tax-exempt interest (Line 2a), plus only 50% of your total Social Security benefit.

Let’s look at a quick example for a single person:

- AGI: $30,000

- Tax-Exempt Interest: $0

- Social Security (Total of $48,000 for the year): Add only half, $24,000.

- Total Provisional Income: $54,000.

You take this $54k provisional income and apply it to a single filer chart with established blocks:

- First $25,000: 0% taxable.

- $25,001 to $34,000 (next $9,000): 50% taxable ($4,500).

- Above $34,000 (last $20,000): 85% taxable ($17,000).

In this example, $21,500 would be reported as taxable Social Security income on their tax return (line 6b). The remaining $26,500 of their total $48,000 benefit is not subject to Social Security taxes at all (line 6a).

Knowing they will owe taxes on $21,500, this senior could file Form W4V (Voluntary Withholding Request). It’s very simple to do and gives you options: you can choose exactly 7%, 10%, 12%, or 22% to have withheld from each check. For high earners, choosing to withhold that 22% is a wise strategic move, as it ensures you don’t face penalties for underpaying estimated taxes. This deduction, however, will make your net Social Security check smaller.

Strategic Pitfalls: Making Mistakes in Benefit Election

Reason number six is a little different. While the previous five dealt with dynamic factors (income changes, premiums), this last factor is a fundamental benefit strategy mistake that results in a permanently reduced check. This is something I would never advise a client to do, but I include it so you are aware of the potential consequence.

This happens when a person claims a lower benefit while a higher benefit is actually available to them. To illustrate, we must look at how spousal benefits work.

Avoiding Strategy Mistakes

A spousal benefit is 50% of whatever your spouse is eligible to receive at their full retirement age (FRA). If you choose to take that 50% before your own FRA, that benefit is reduced by a penalty far heftier than if you were taking your own retirement benefit early. This permanent reduction is substantial.

If your spouse takes and is getting $4,000 at their FRA, you would be eligible for 50% ($2,000) at your own FRA. If your own retirement benefit is only $1,000, but the spousal benefit is $1,500 at the same age, you would simply take the spousal benefit for your entire life. You can only receive one benefit (retirement, spouse, or survivor).

What some people fail to realize is that you do not have to file for your own lower benefit if a higher spousal benefit is available. You take the spousal for higher amount. I put it up here because sometimes people want to take their own, but you can’t have both. So, if your own benefit is permanently less, you should not file for it. Taking the wrong one can mean your monthly check is permanently less than what it should be.

Ways to Increase Your Social Security Benefit

To close, while a check decreasing is disappointing, it is important to remember the flexibility inherent in the Social Security system. There are many unique strategies designed specifically to increase your benefit. I encourage my clients to take advantage of these different options:

- Switching Own Benefit to Spousal: If you take your own benefit early, but your spouse later hits FRA and takes their much higher benefit, you can file a new application to “increase” your check to receive the spousal amount.

- Switching Benefit Types to Survivor: If you are taking a benefit and your spouse dies, you can always increase that benefit to the survivor benefit if it is greater. This survivor benefit is 100% of whatever that spouse was eligible for when they died, including all their COLAs.

- Survivor Benefit for Widows (Age 60): A widow or widower can start taking a special survivor benefit at age 60. This will be subject to an earnings test and reduction, but you can take that $3,000 benefit while letting your own retirement account grow until age 70, where it may be worth $4,000. You then stop taking the survivor benefit and start taking your own, increased retirement check.

Navigating the New Social Security System

Navigating this system is complex, but a decrease is usually correctable or a sign you are using other critical services like Medicare B. It is important to remember how often things change. The Social Security Administration made some major changes on March 7th that greatly altered how seniors navigate the system. It is critical to stay informed, track your income, understand Medicare’s timelines, and review your tax returns. Doing so ensures you can either prepare for a reduction or, even better, appeal it.

💡 Frequently Asked Questions (FAQ)

Q1: What happens if Social Security overpays me, but the error was their fault?

A1: Even if the error was purely SSA’s fault, you are still legally responsible for repaying that money, as you were technically paid incorrectly. Your check will decrease until the overpayment is recovered. However, when the error is not your fault, you have a stronger case to request a payment plan that avoids hardship or file for a full waiver if repaying it would be financially devastating.

Q2: My 2024 income was high, but I fully retired last year. Will I still have to pay the high IRMAA surcharges in 2026?

A2: Yes, initially you will, because Social Security uses a automatic two-year look-back period (they are looking at 2024 for 2026). However, you have the right to challenge this immediately. Because “Work Stoppage” is one of the recognized life-changing events, you should file Form SSA-44 as soon as you retire. Provide them with proof of your work cessation (such as a termination letter) and a projection of your new, much lower income for 2026. This will allow you to get IRMAA removed and lower your monthly payment.

Q3: Can I choose any amount to have voluntarily withheld for taxes from my Social Security check?

A3: No. Unlike a standard employment W-4 where you can set extra withholding to a specific dollar amount, Form W4V gives you only four specific options for voluntary withholding: 7%, 10%, 12%, or 22% of your total benefit payment. You must select one of these specific percentage options to start, change, or stop the withholding. It is a powerful tool to avoid underpayment penalties if you have higher retirement income.

🌿 Weekly wellness, health & beauty insights — straight to your inbox

Free subscription · Cancel anytime